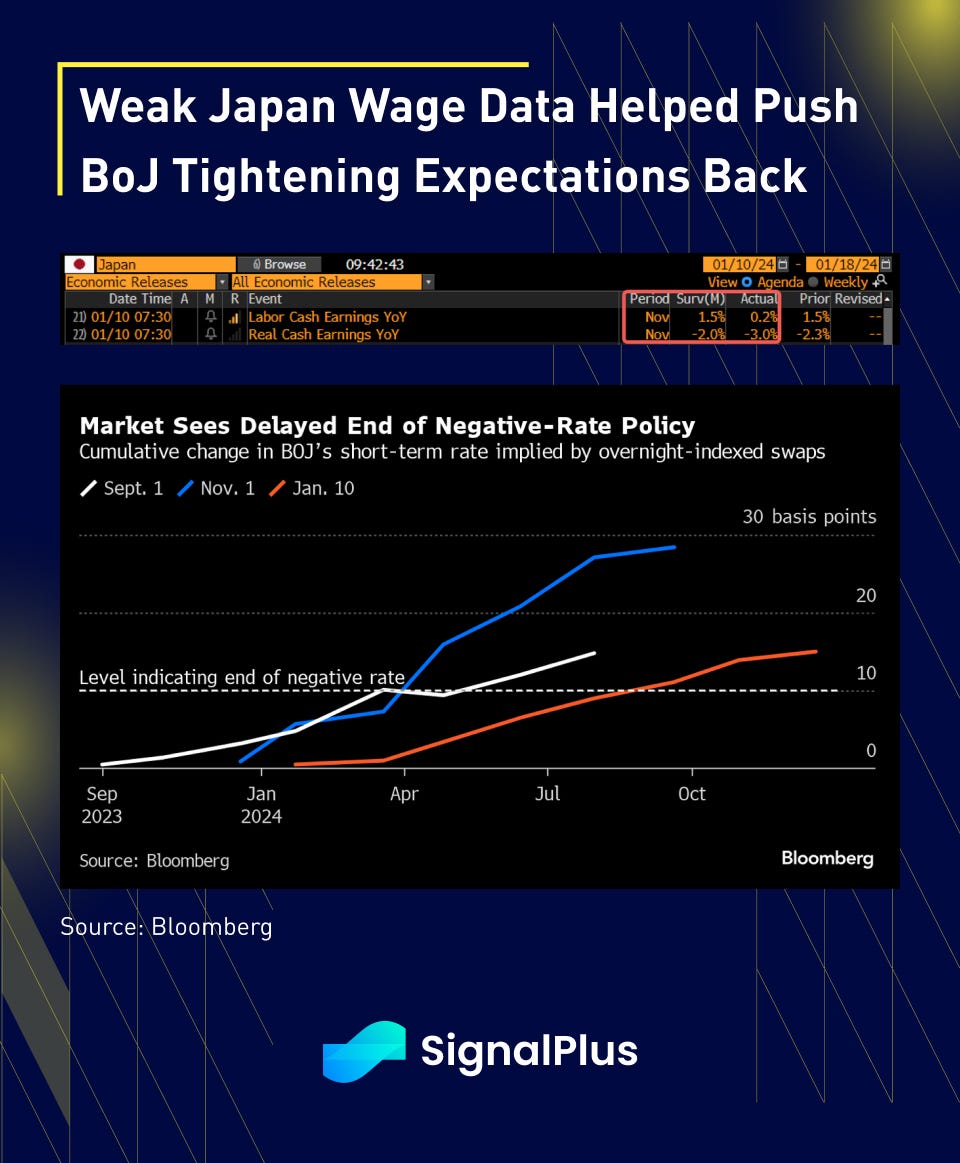

An earlier miss in Japan wage growth (-3% YoY vs -2% expected) continued the global dovish pivot, as the BOJ is now expected to end its negative rate policy closer to September rather than in April. The JPY sold off back to 146, and the Nikkei has climbed to 35-year highs, and on the verge of eclipsing its record highs from the much maligned ‘bubble-era’. Japanese stocks have once again been the standout outperformer YTD, ratcheting nearly ~5% gains and even ~1.5% on an FX-adjusted basis, far outperforming other developed markets globally (US flat, Europe -1.7%, China -5.5%).

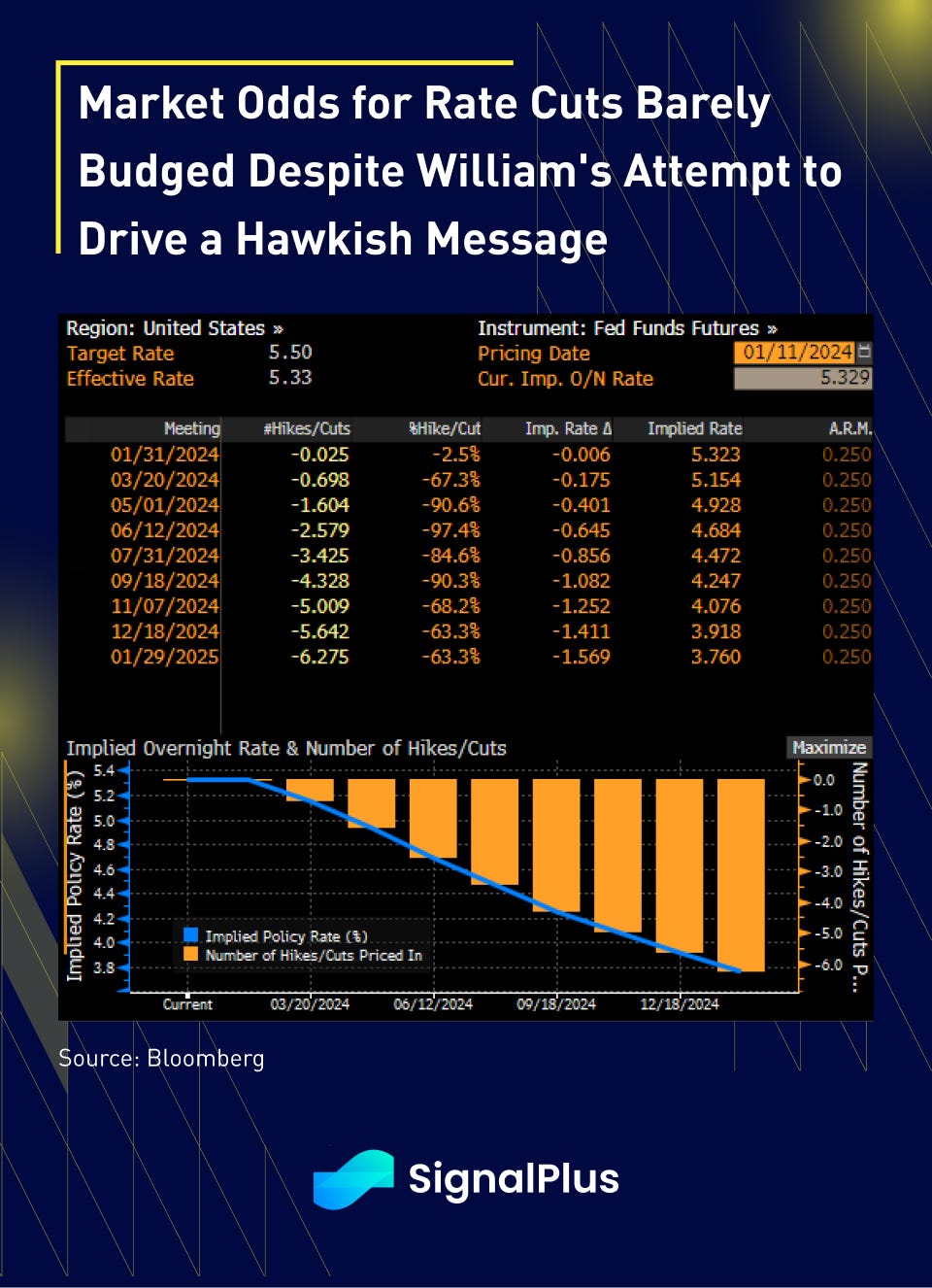

Activity was healthy across most asset classes, but price action was well contained on a lack of market moving data, and traders doing some final position rebalancings ahead of today’s CPI. Fed’s Williams tried to inject some hawkish messaging on the Fed’s balance sheet, stating that they “don’t seem to be close to the point” on when the FOMC will “stop the decline in the size of the balance sheet”, and that “I expect that we will need to maintain a restrictive stance of policy for some time to fully achieve our goals, and it will only be appropriate to dial back the degree of policy restraint when we are confident that inflation is moving towards 2% on a sustained basis. However, the market is well immunized against these deliberate but feeble attempts to tighten financial conditions, with the March meeting still pricing in nearly 70% of a cut.

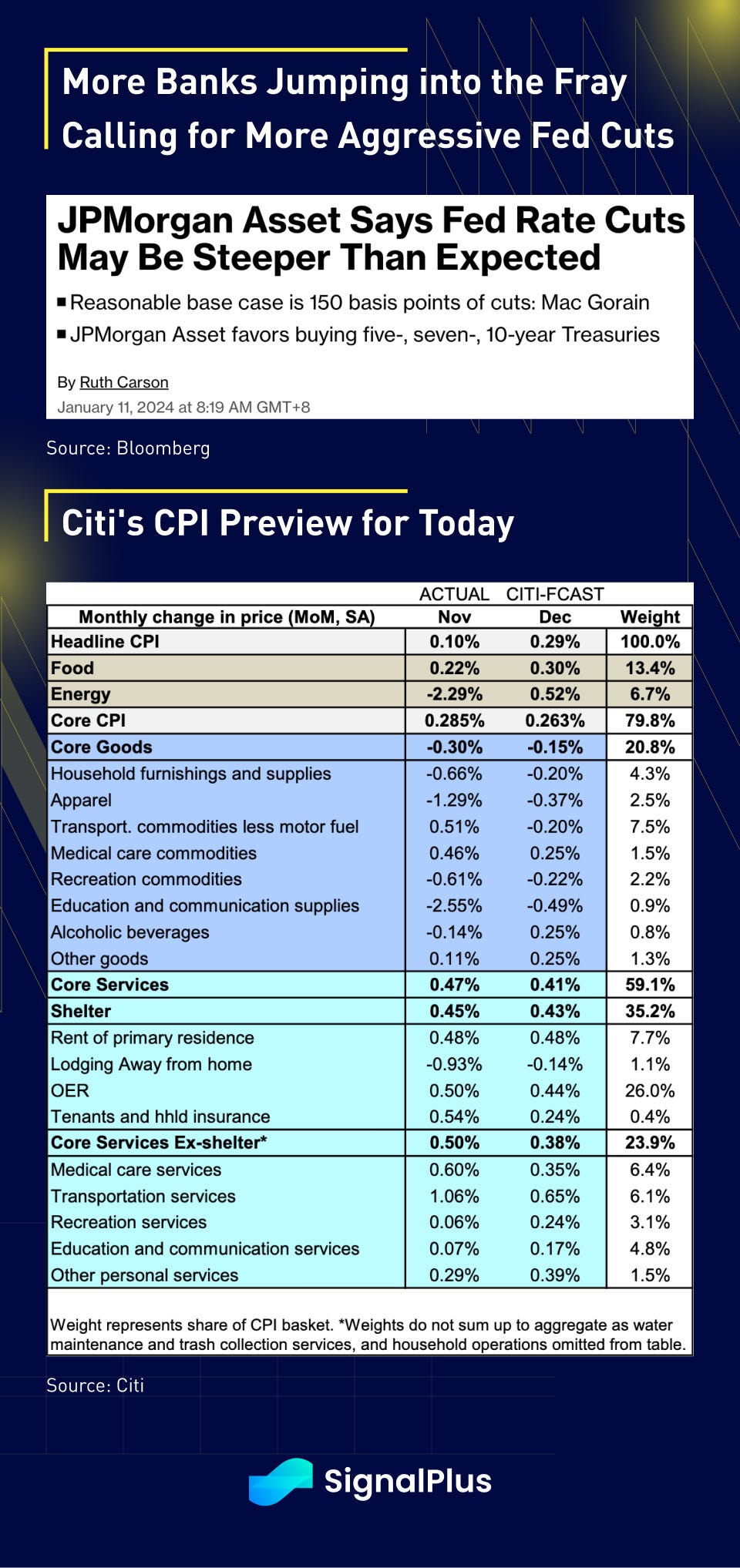

Furthermore, similar to the comments from PIMCO we touched on earlier, we are seeing more large financial institutions making explicit calls for steeper than expected cuts in 2024, with JPM the latest to jump into the fray calling for the market’s 150bp of cuts as merely a ‘central case’, and that a bad economic outcome would see “quite a bit bigger than that”. So after the Fed pivot, should we be expecting to see a Wall Street pivot as well as a follow-through? Today’s CPI release should be a key piece to that narrative depending on where it ultimately comes in (0.3% Core, with strength expected in services and offset by soft goods prices).

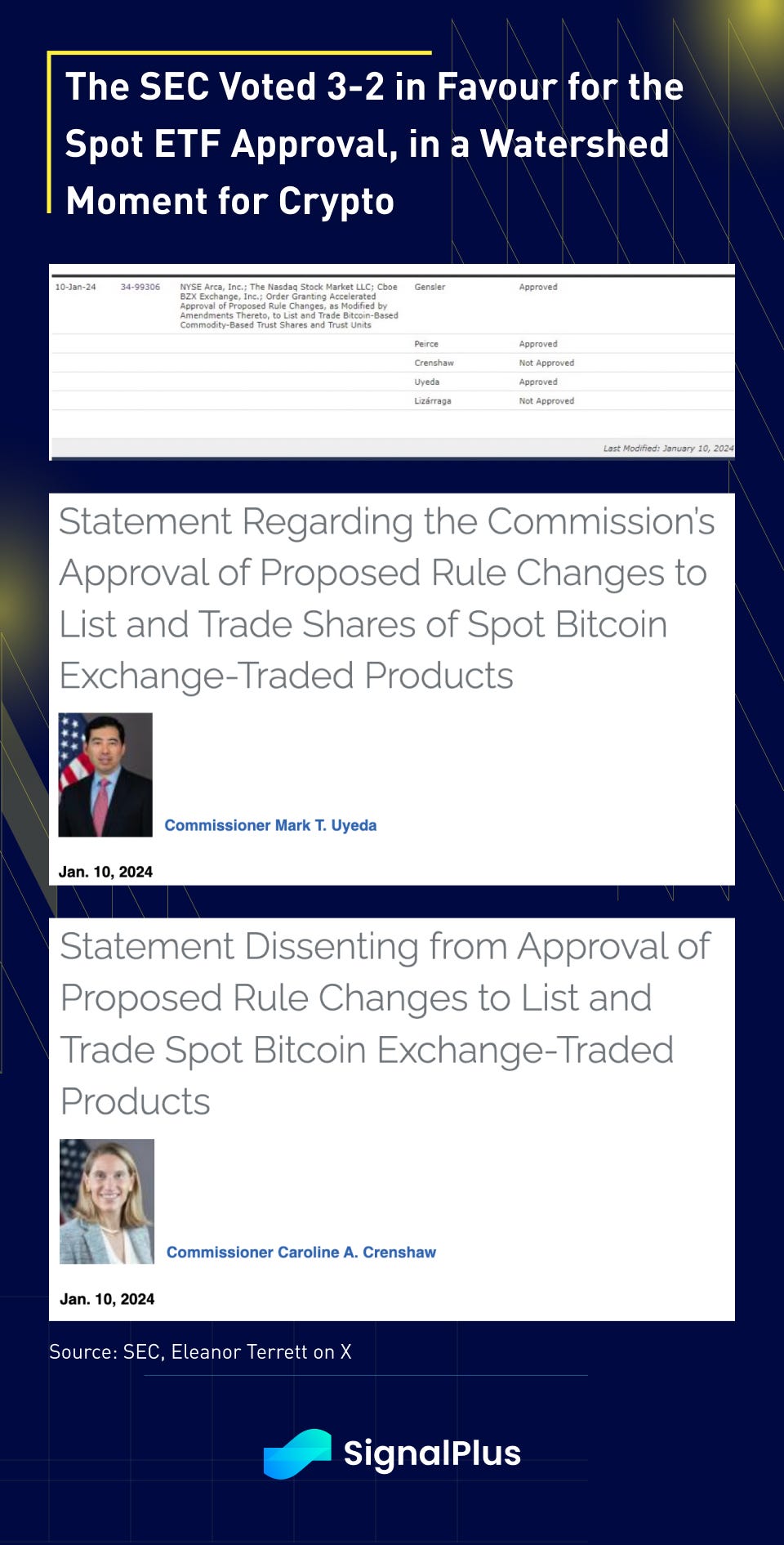

In crypto, the big day is finally upon us, with the SEC finally approving the first batch of (11) eligible spot ETFs including offerings from Blackrock, ARk 21, Fidelity, Invesco, and VanEck. The vote was apparently a close one, passing 3–2 with SEC Chair Gensler acting as the deciding vote with his blessing (say what?), while Republican Commissioners gave dissenting votes.

Naturally, the SEC Chair would not let the decision go gentle into that good night, and caveated the statement with reiterations that they “did not approve or endorse bitcoin”, and that bitcoin remains “primarily a speculative, volatile asset that’s also used for illicit activity”, and that today’s actions “in no way signal the commission’s willingness to approve listing standards for crypto asset securities”, amongst other push-backs. Just in case we weren’t clear how he really feels about the issue!

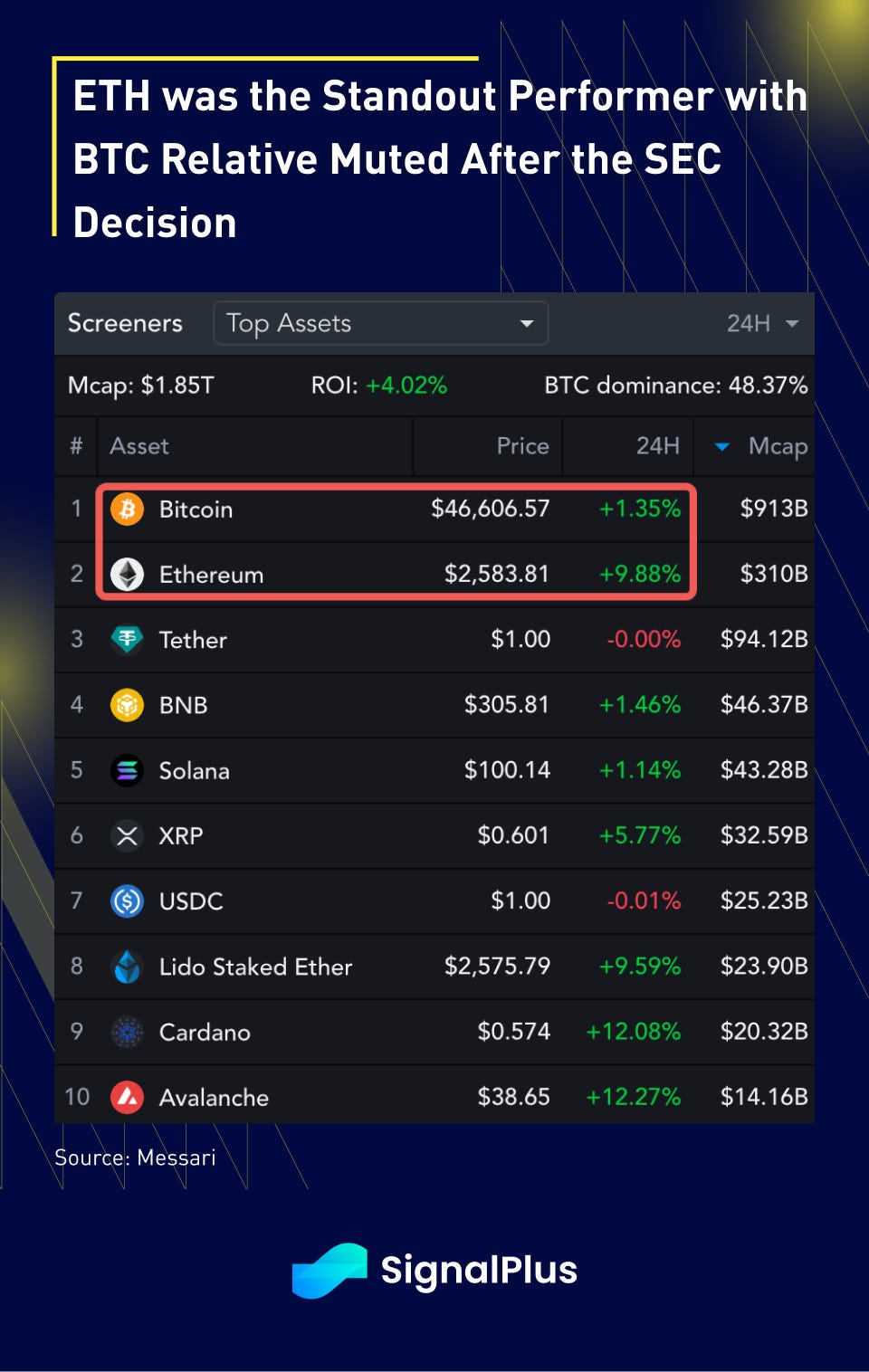

Price action has been relatively muted, with spot still sub $47k without a lot of ‘selling the news’ or FOMO-ing into the asset, as perhaps yesterday’s ‘hacked’ tweet already did released a lot of the gamma risk ahead of time. ETH was the standout performer following a long period of underperformance vs BTC, as the focus will now be on Ethereum-based spot ETFs, so we get to do this merry-go-round once again with the SEC in the near future.

And on that, a warm welcome to crypto to our dear TradFi friends, and may you stay and look-around for a long time!

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Comments