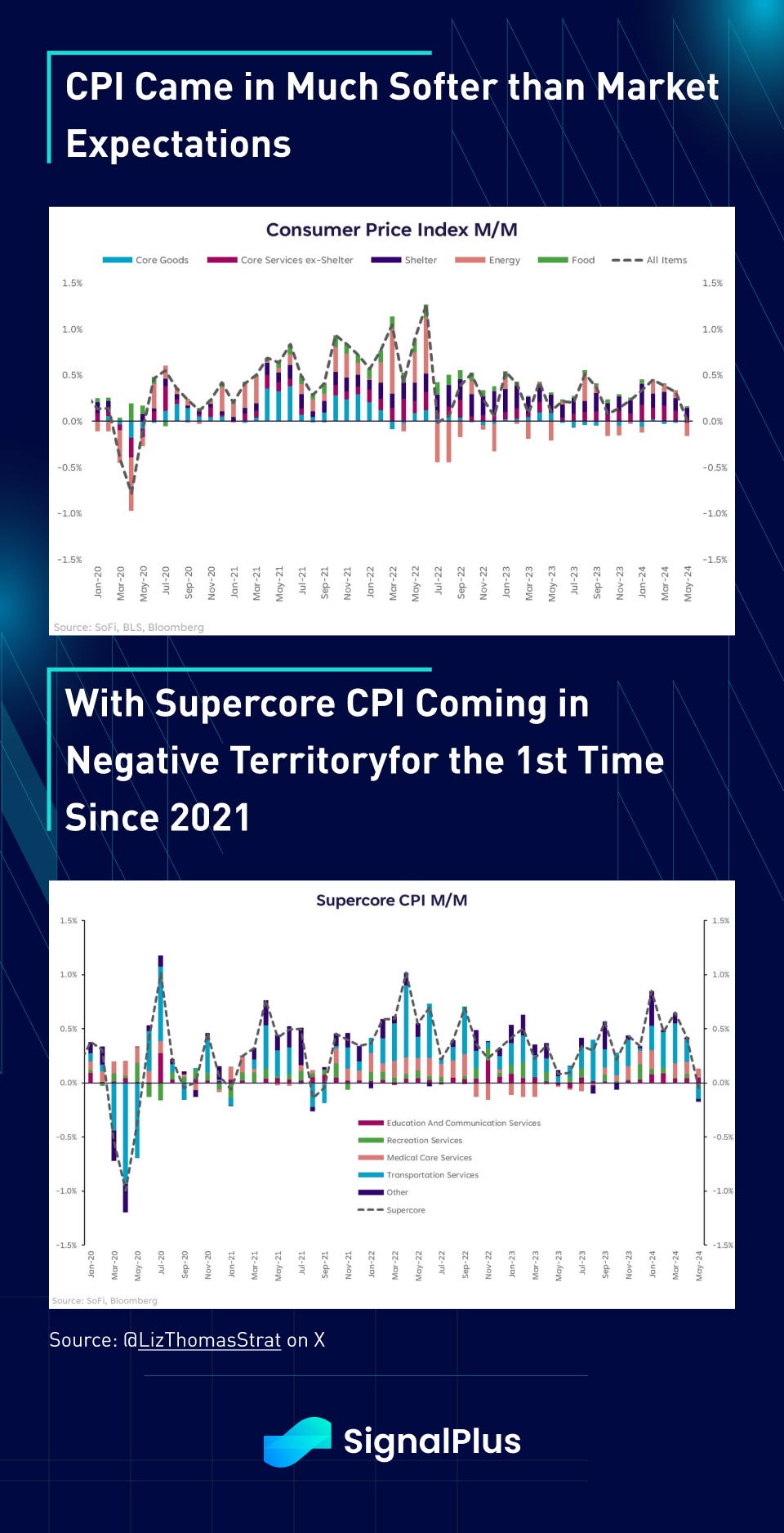

The big macro double-header day was finally upon us, and things certainly didn’t disappoint. CPI started us off with a much softer than expected print, with core rising 0.16% MoM (lowest since August 2021) vs consensus estimates of 0.3%, with particular softness seen in the ‘supercore’ CPI which managed to hit negative territory in May. Services spending fell, good prices were flat, and shelter inflation rose but stayed within manageable territory. Post CPI, Wall Street economists were quick to update PCE forecasts from 2.8% down to 2.6%, and moving in the right direction towards the Fed’s long-term target.

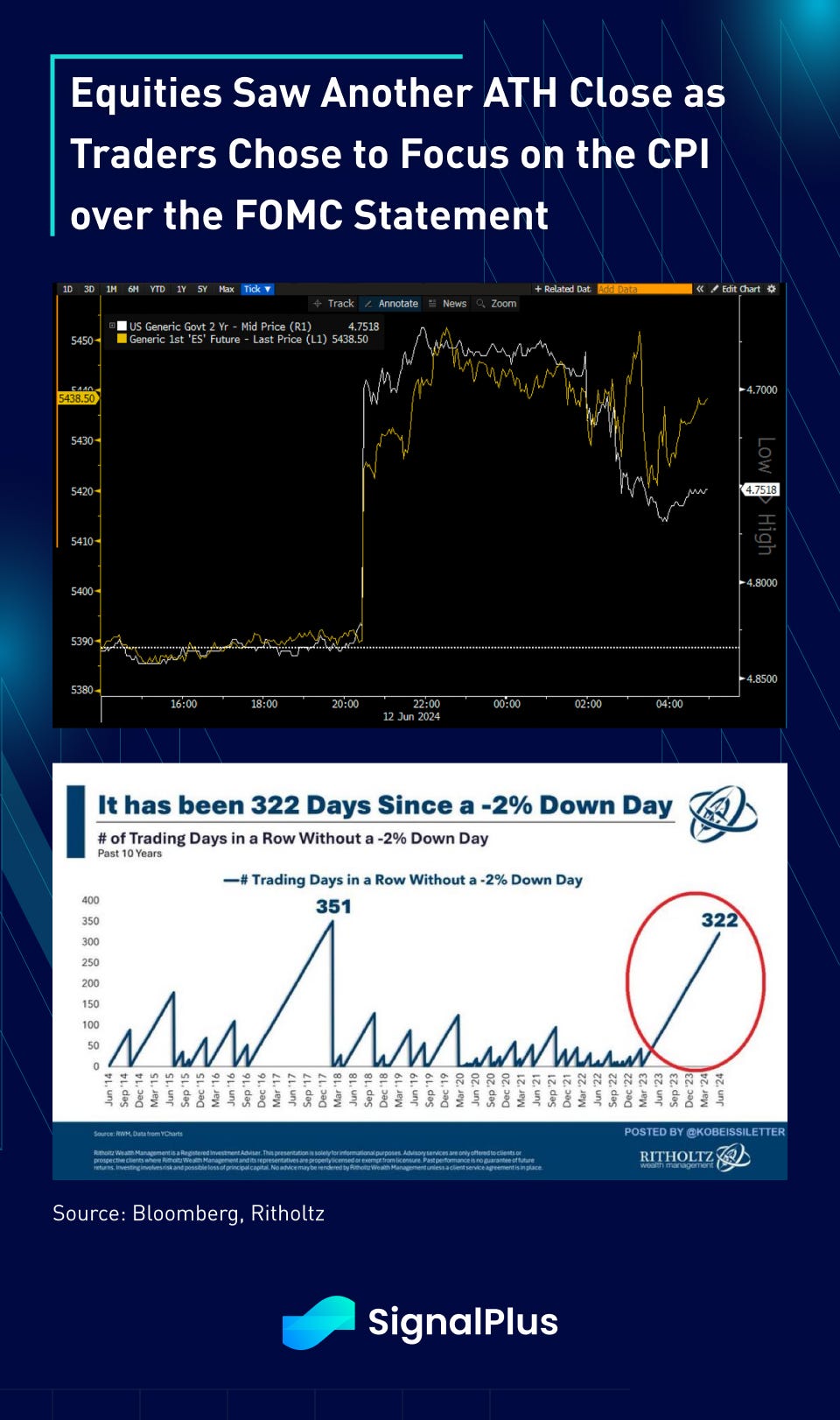

Macro reaction was violent, with treasuries bull-steepening led by 2yr yields dropping as much as 17bp. The December FOMC meeting date has priced in as much as 51bp at the extremes. Equities saw a multi-sigma move with SPX and Nasdaq both rallying +1.5% on the print, breaking record highs as markets entered into the 2pm FOMC expecting a dovish outcome.

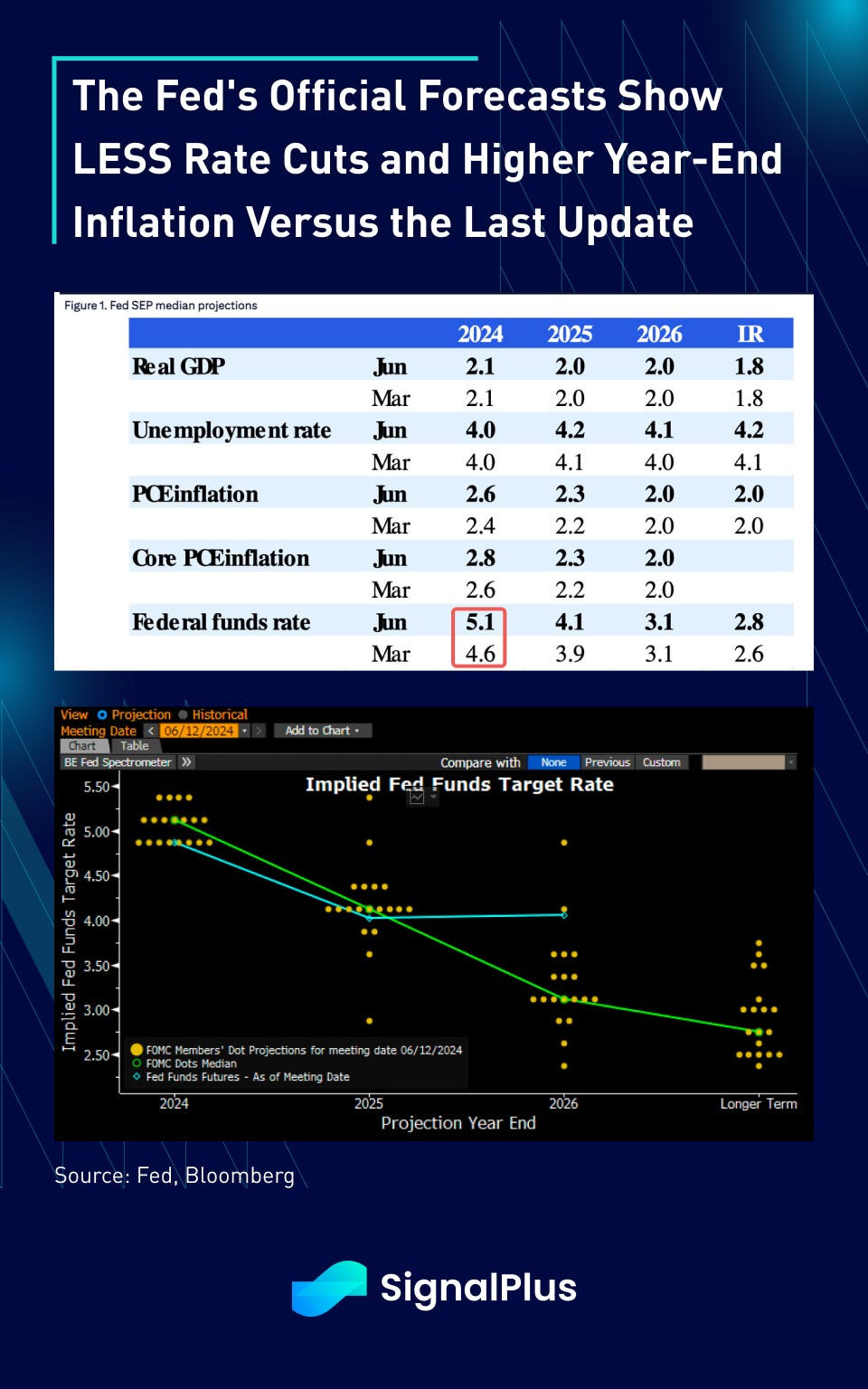

Interestingly, the initial FOMC statement and ‘dot-plot’ arrived with a bit of a hawkish shock, with the latest Fed forecasts showing just ONE rate cut in 2024 versus THREE from earlier. Furthermore, core PCE inflation is projected to end the year at 2.8%, higher than the 2.6% previously.

Naturally, Chairman Powell spent most of the press conference trying to wiggle the narrative back into dovish territory, explicitly trying to downplay the importance of these projections. Powell went as far as outright stating that “most” officials” did not include yesterday’s soft CPI into their forecasts, so that they are already effectively ‘stale’ to some degree. Talk about a stick save.

Furthermore, Powell noted that the labour market has moved back to a similar state just before the pandemic, with job openings, quit rates, and a returning supply of workers showing signs of normalization again. On the economy, the Fed sees growth continuing to happen at a solid pace and that the officials are “kind of seeing what [they] wanted to see, which was gradual cooling in demand”. Finally, he also made sure to stress that the Fed is paying attention to downside risks and wants to preserve an economic soft landing as a priority.

When all is said and done, Bloomberg noted that Powell mentioned inflation 91 times vs 37 times of the labour market, suggesting that pricing pressures remain top of mind. Equity markets took the cue and decided to re-focus back on the softer CPI from before, leaving us close to ATHs at around 5438 on the SPX, while 2yr treasuries settled at ~4.70% and 10y at ~4.3%, both around the lows of the week. The SPX is now on its 2nd longest streak in history without a -2% down day. Just another month until we can set another risk-on record for this cycle!

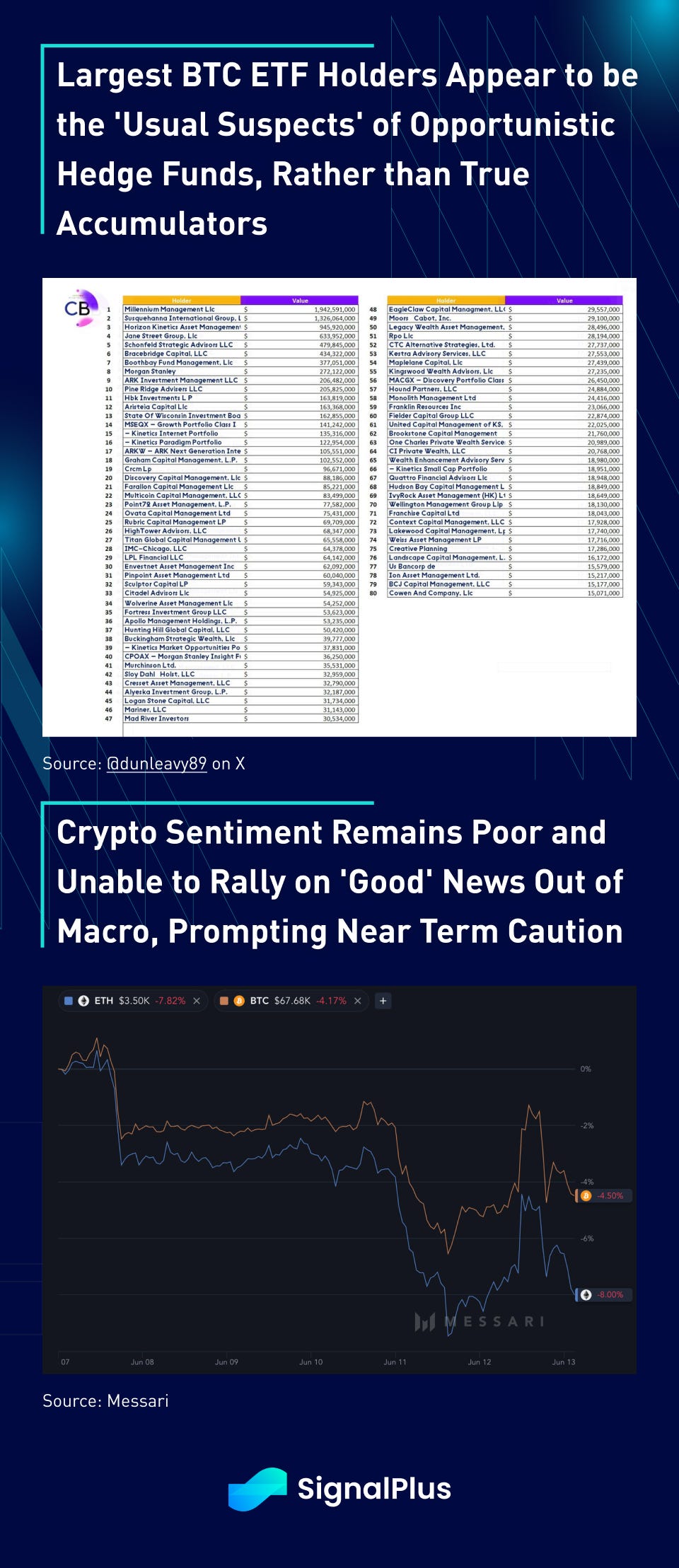

Crypto prices struggled all week despite the overall macro strength, as off-sided long positions and disappointments about the ‘mix’ of BTC ETF holders are raising questions on how much the YTD inflows are based off accumulation rather than relative-value or ‘basis’ trading. Bitcoin has struggled to break $70k and Ethereum is down 8% on the week as the ETF approval catalyst has faded, while concerns about dwindling fees and competition from L2 continue. Technicals look a bit challenging at the moment, with markets feeling susceptible to a long-overdue reversal in equity sentiment in the near term. Good luck!

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments