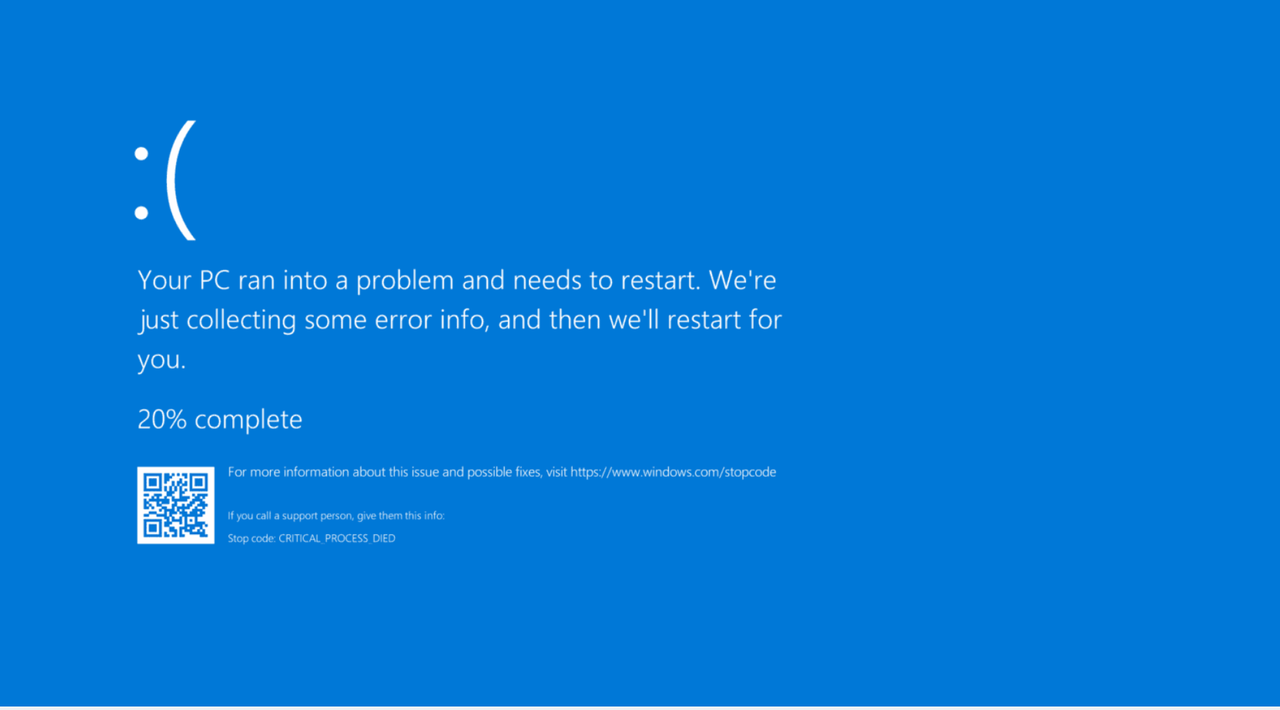

The tech world was rudely reminded of the perils over over-centralization and reliance on singular nodes, as a botched update from cybersecurity giant Cloudstrike wrecked havoc across global systems, knocking out enterprise logins, banking systems, commercial flights, and countless other systems running of a Windows backbone.

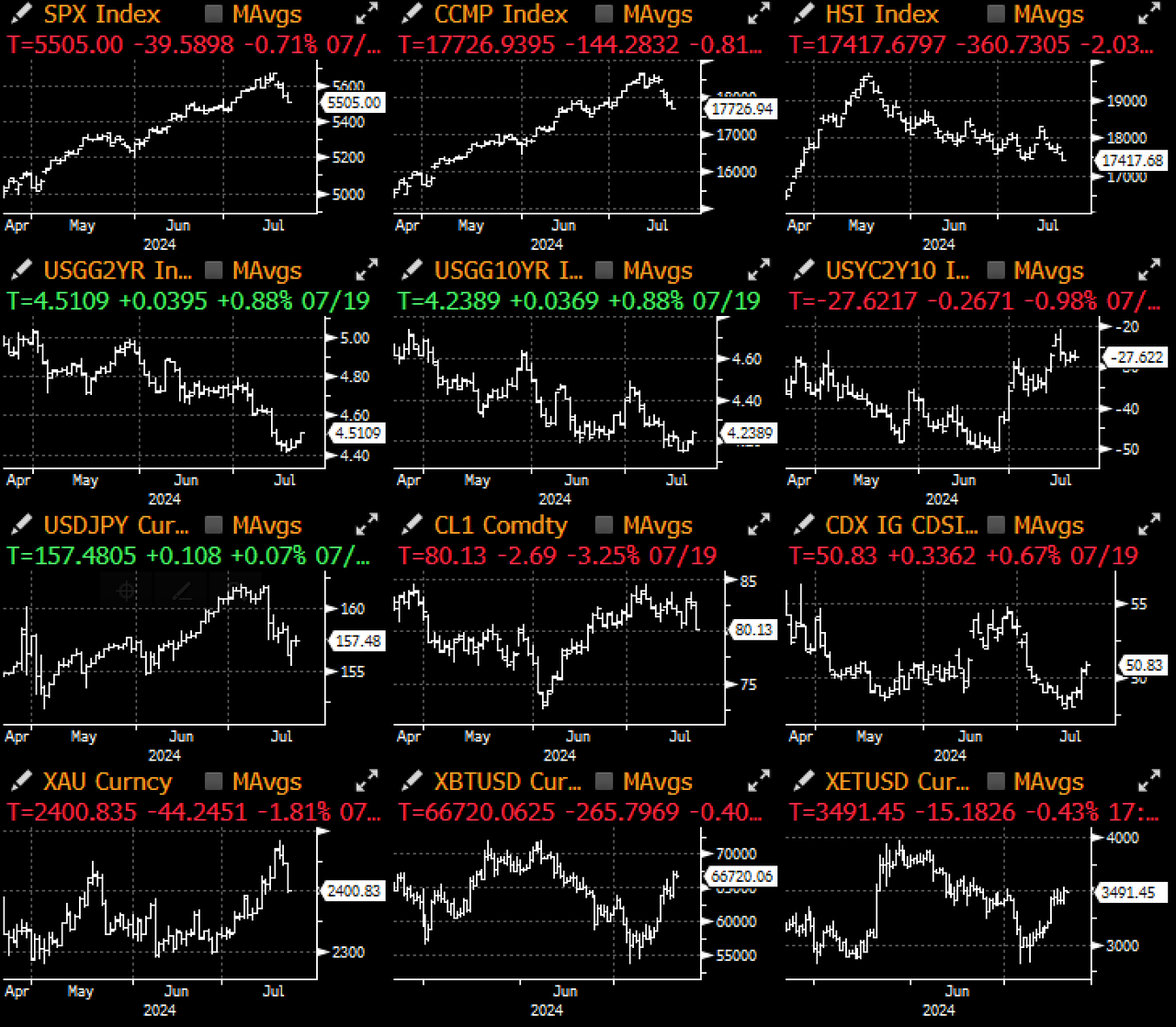

Brushing aside initial scares of a more nefarious security attack, equities markets struggled nevertheless with Nasdaq trading off -1% on the day and Cloudstrike cratering -15% at the open. The weak Friday session continued a forgetful week where equities struggled after reaching new ATHs just ahead of the latest US election drama.

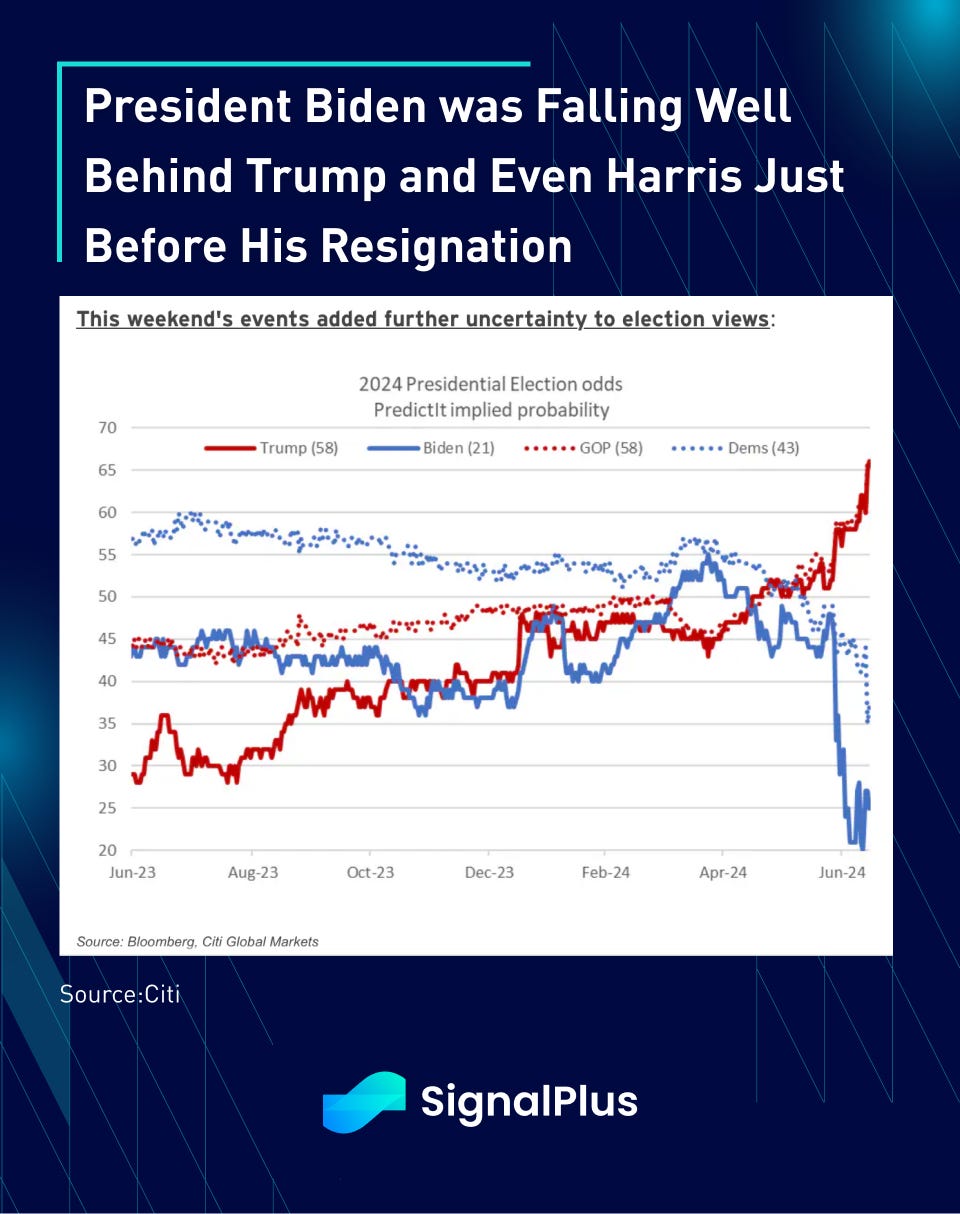

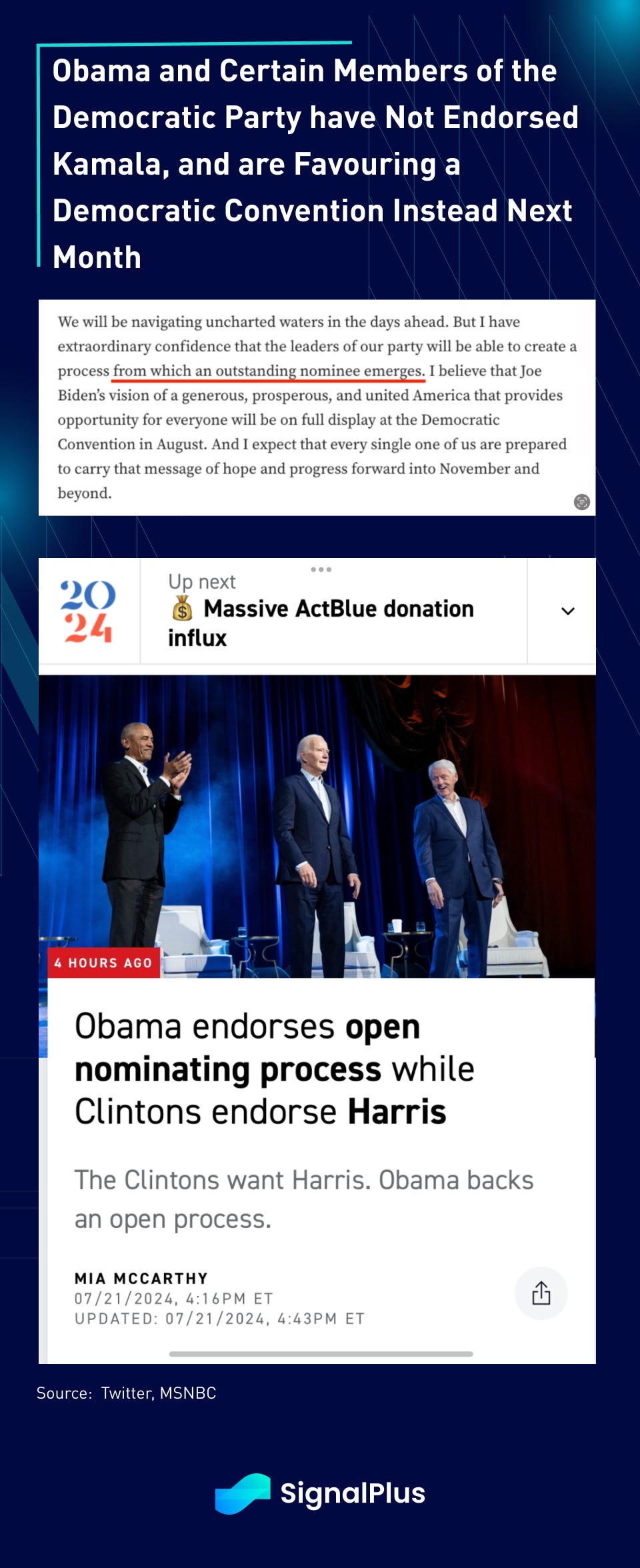

In the immortal words of everyone’s favorite IT manager — ‘have you tried rebooting?’ — a fresh start appears to be a panacea for all our ills, including the democratic process. While the timing was rather abrupt, but President Biden has finally stepped aside to allow VP Harris to take the helm; however, former President Obama and other party members have stopped short of endorsing Harris, and have indicated a preference towards a Deomcratic convention next month, adding further uncertainty to what has already been a wild election cycle.

While equities were largely euphoric over the prospects of a Trump 2nd term, a certain amount of self-reflection had started to set in with chip stocks starting to falter along with long-dated treasuries (on debt-driven stimulus plans). In a scathing interview to Bloomberg, Trump showed strong disdain on the Taiwan-China issue by expressing:

“I mean, how stupid are we? They [Taiwan] took all of our chip business. They’re immensely wealthy. I don’t think we’re any different from an insurance policy. Why are we doing this? — Trump

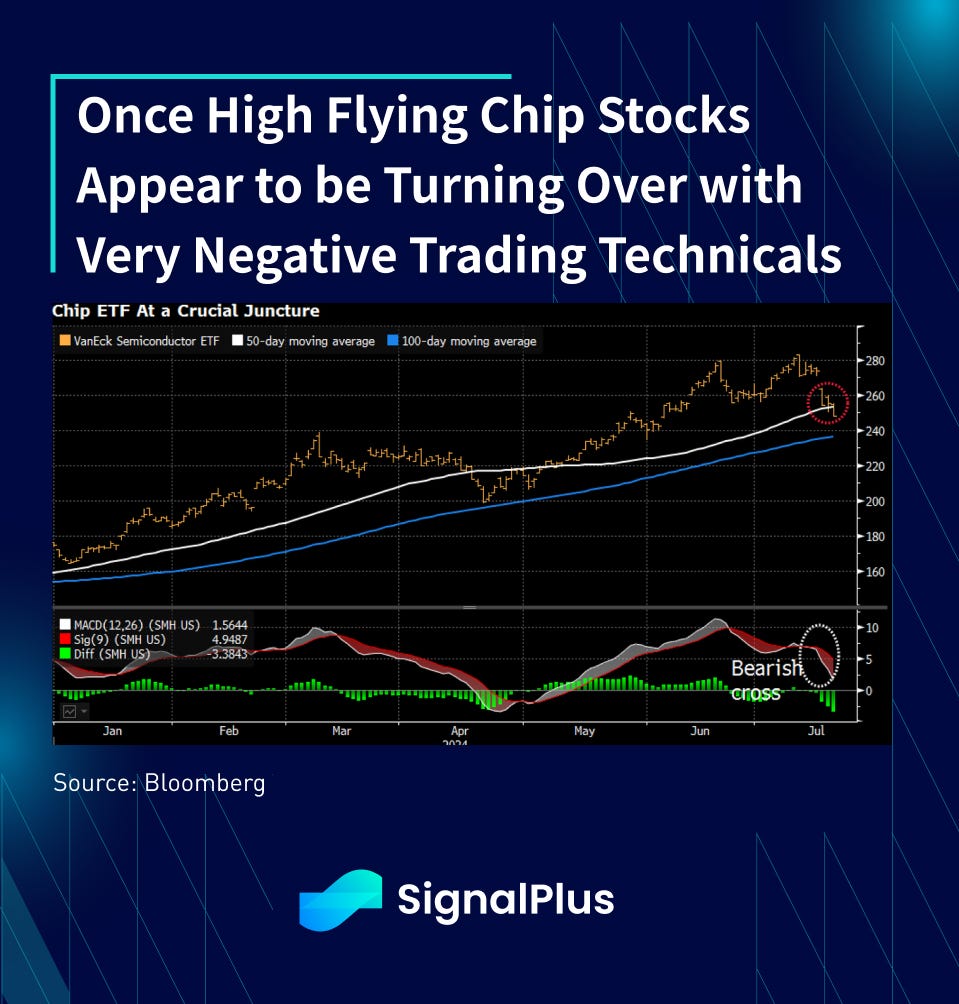

To make matters worse, even the Democrats were contemplating whether to impose even stricter chip sanctions on China, doubling down on their earlier efforts. In response, TSMC sold off ~4% post the remarks and semiconductor stocks fell ~7% on the week, with the latter breaching the 50d MA and short-term stochastics falling into bearish territory.

While it awaits to be seen how US markets will respond to this weekend’s news, but Friday was one of those ‘sell everything days’ where every major asset class was down except for Bitcoin. Stocks, bonds, gold, oil… everything was in the red and the commodities index saw the weakest close since March as optimism over global economic growth is waning.

According to Bloomberg data, only 4% of all trading sessions over the past 40 years saw all the major US equity indices, oil, gold, and treasuries sold off in unison. A mere 0.5% of days saw this happen twice in a row, and a near non-existent 0.03% of sessions (3 times) saw this happen on three consecutive days, and all of which took place during hawkish Fed periods.

The bearish developments were not limited to just the US. Greater China equities dipped noticably as China’s Third Plenum underwhelmed investors with a lack of ‘shock and awe’ stimulus, and didn’t show any remarkable change in direction despite the ongoing economic malaise.

Rising threats of US tariffs will continue to loom large over investors’ minds, with GS stating that a 10% tariff could spark a trade war retaliation, causing US inflation to rise by over 1% and possibly forcing the Fed back towards consecutive rate hikes.

To exacerbate matters, as if the idea of a further trade war and debt-fueled stimulus is not enough, Trump has also explicitly stated his preference for a weaker USD, in particular against China and Japan, by reinforcing his preference for bringing manufacturing back to America.

I think manufacturing is a big deal, and everybody that runs for office says you’ll never manufacture again. We have currency problems, as you know. Currency. When I was president, I fought very strongly and hard with President Xi and with Shinzo Abe… So we have a big currency problem because the depth of the currency now in terms of strong dollar/weak yen, weak yuan, is massive. — Trump

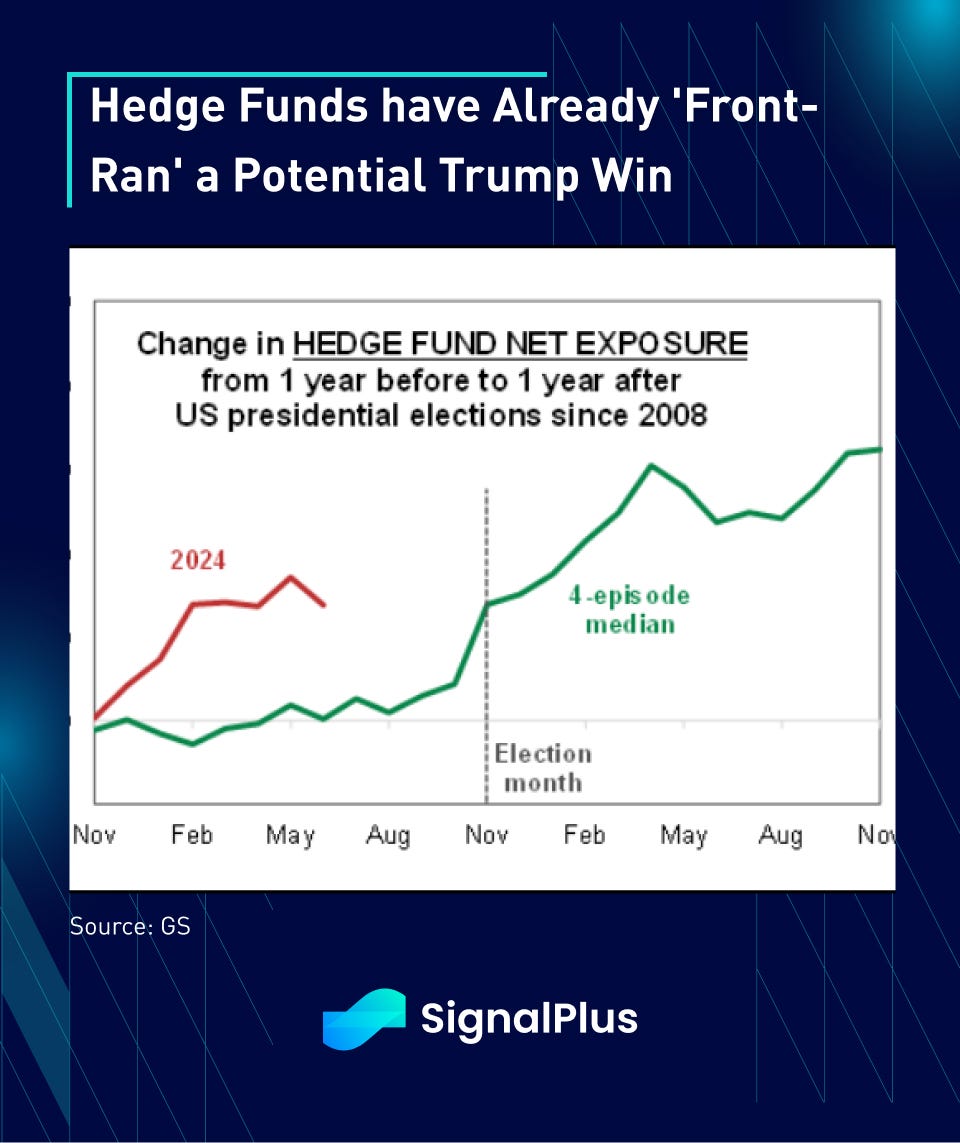

Is it any wonder that investors are almost universally bearish long bonds on a Trump 2nd term? And how will inflation pressures respond to a backdrop of higher fiscal spending / lower USD / higher trade prices / rising bond issuance?

Somewhat concerningly, ocean freight costs have already been rising under the hood, despite the conclusion of pandemic-led supply constraints, with the Baltic Dry rising to this 83rd %-percentile versus the past decade.

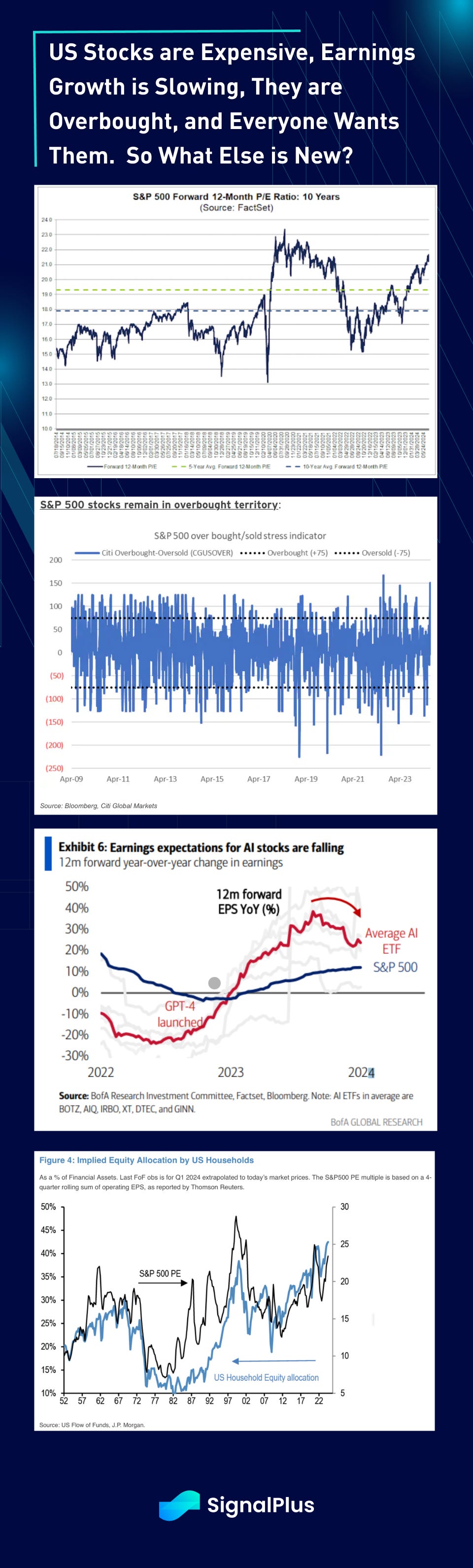

In the meantime, there’s not much new insight on US equities. Stocks are expensive on a forward PE basis (>21.5x) and against most measurement metrics. They remain overbought and have been overbought for weeks, and US household allocations are at historical highs and even above the 1999 dot-com highs. At the same time, AI stocks earnings growth is expected to moderate in the upcoming quarters, but will continue to drive the lion’s share of overall index earnings.

As such, we remain in this highly uncomfortable state where investors and performance chasers are forced into equities at a late economic cycle, with worsening geopolitics, rising valuations, and ever worsening risk-reward ratios. We have always expressed to our readers that equities are a coincident indicator (at best), and are most certainly not forward looking. However, the macro graveyard is also filled by equity bears that have suffered untold losses from trying to short equities (including 2023–24), so keep your bullets dry for a very wild few months with the announcement of the next Democrat nominee, 1st expected Fed cuts, escalating trade war, and US elections mixing as a highly volatile cocktail.

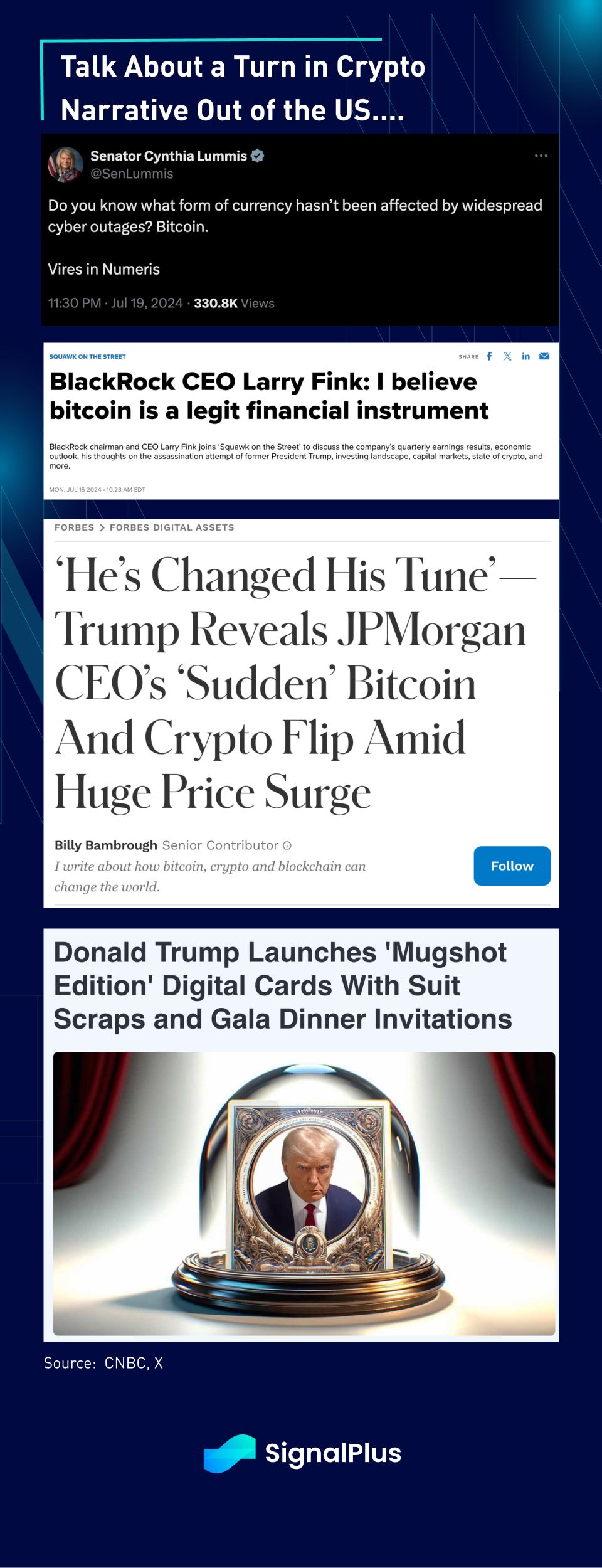

Over in crypto, what a change a month can take. After cratering to $54k a few weeks ago on govt-based selling and putting the entire bull-run at risk, a pro-crypto Trump administration flipped BTC on its head, staging a rapid squeeze back up to $68k with investors extremely under positioned following the earlier crash.

A series of bullish (opportunistic?) rhetoric from the Trump campaign, US senators, Blackrock’s Larry Fink and even JPM’s own Jaime Dimon have done much to change the US narrative, and we can be sure that TradFi’s influence in crypto will only continue to grow regardless of which is running the White House over the next 4 years.

On the regulatory side, positive headlines are also starting to surface with Ripple’s CEO expecting a positive legal resolution ‘very soon’, and the SEC-approved ETH ETFs scheduled to start trading this week.

This is reflected in the ETF inflows, which have reaccelerated to the upside over the past week, seeing over 1bln in new inflows over the past 5 days.

In terms of market sentiment, perpetual funding rates are back close ot flat, implied vols are drifiting lower as we settle back into the 60–70k range, but trading houses are reporting large upsized in year-end BTC $100k calls to bet on a late YE rally. Will the 3rd time be the charm? Let’s keep our fingers crossed.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments