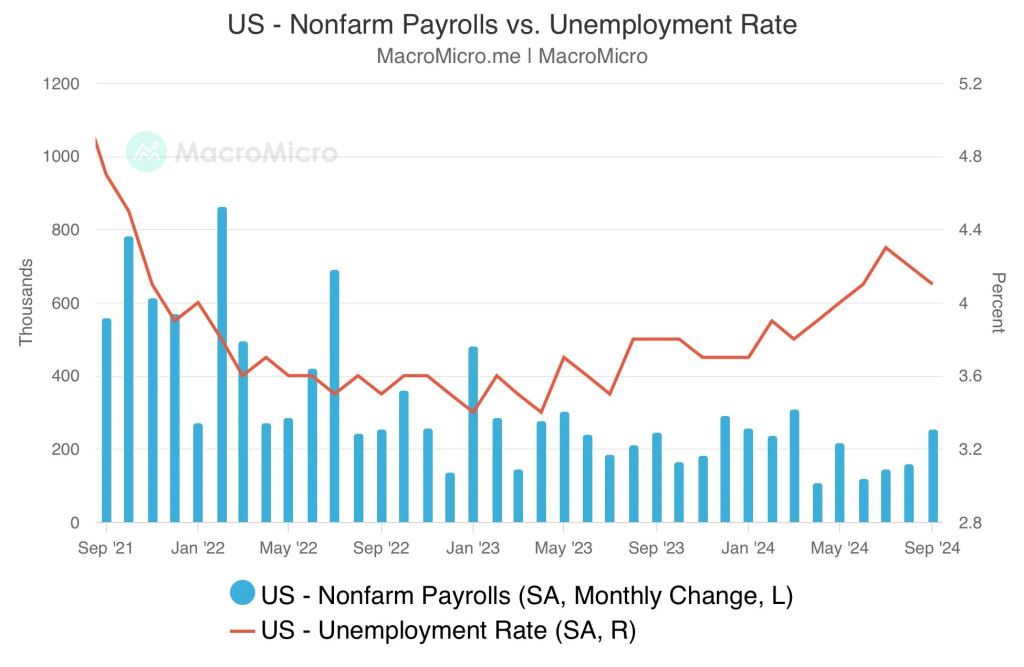

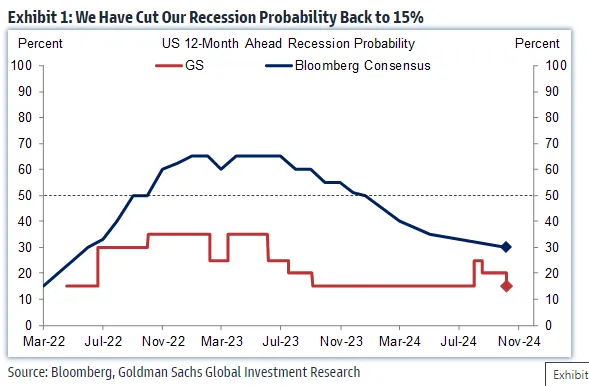

The NFP data released last Friday was very strong at +254k. There has been a lot of debate about whether the NFP adjustment is a government manipulation or not… but even so, it is definitely a very strong data. Yes, the US continues to add jobs. This has lowered Goldman Sachs’s recession probability from 20% to 15%. This is consistent with my view that there will be no recession in 2024.

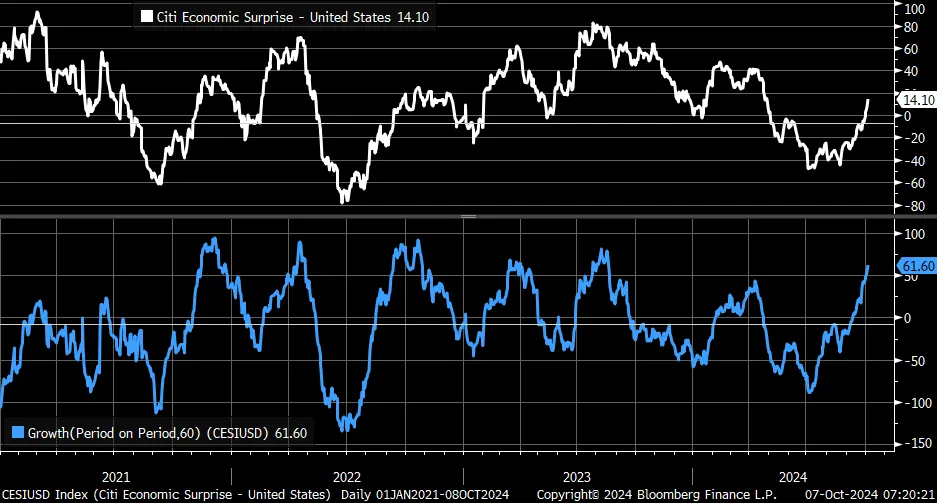

The Citi Economic Surprise Index has continued to rise since its low. While this data does not reflect all situations perfectly, it does indicate that actual figures have often been more optimistic than expectations for economic data.

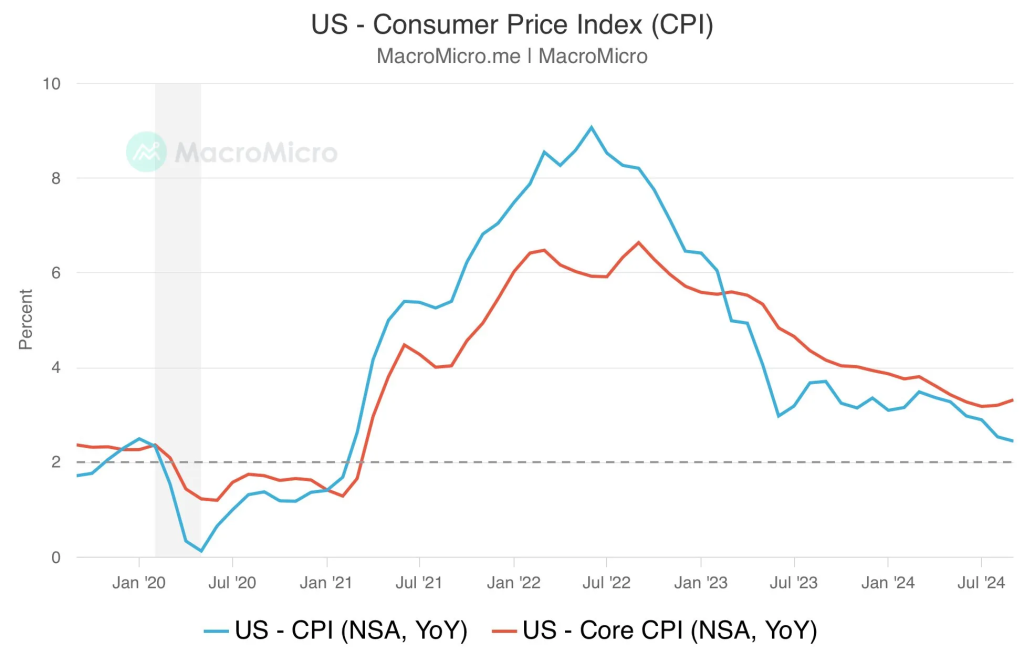

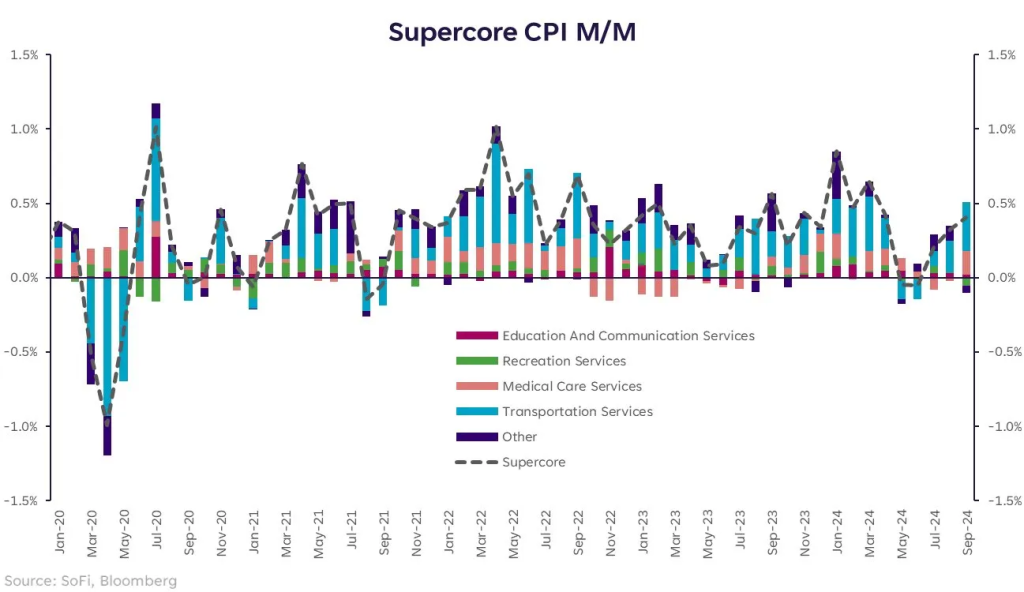

CPI yesterday was less than optimistic. The headline showed the disinflation trend continuing at 2.4% (YoY), but the core was up 3.3% (YoY) from the previous month. The supercore CPI is continuing its upward trend, which is a big concern. At the September FOMC, Powell said that it is too early for the Fed to declare victory on inflation because the supercore CPI is rising.

There is a lot of debate among market participants about the reacceleration of inflation, but I think it is too early to judge. To be precise, we will need to confirm more data over several months. I agree with the point that there is a possibility of reacceleration of inflation in the current cycle, when central banks around the world are cutting rates. As I said a few weeks ago, inflation is more likely to rise again than to fall sharply, but I still think that the time for market participants to worry is 2025, not 2024.

This data is from August and the Fed’s next rate decision is in November, so I don’t think this CPI will have much influence on their rate decision. There’s a lot of debate about whether there will be a rate cut in November after the CPI data, but as of now, I think they will cut by 25bp. Yes, it’s clear that the FOMC uncertainty in November has increased. The data that will come up will be more important.

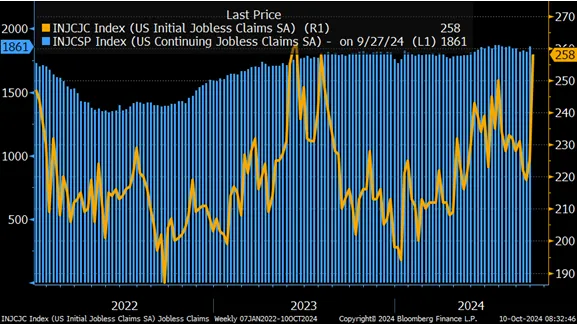

The actual market impact yesterday was likely related to the claims numbers. The data went up significantly yesterday. There is a lot of debate about this data. [There may be a hurricane effect vs. a hurricane effect, but overall they all rose] Yes, I don’t know the answer. What is clear is that we need to watch additional data. Everything is a matter of speculation. But I agree that for what it is, it’s bad data.

FED’S WILLIAMS: EXPECTS INFLATION TO WANE TO 2.25% THIS YEAR, CLOSE TO 2% IN 2025

FED’S WILLIAMS: SEES 2024 GDP BETWEEN 2.25-2.5%, 2.25% AVERAGE OVER NEXT TWO YEARS

FED’S WILLIAMS: SEES UNEMPLOYMENT AT 4.25% THIS YEAR AND AROUND THAT IN 2025

Currently, the Fed is likely to focus more on growth and the labor market than on prices in determining interest rates, unless inflation rises sharply.

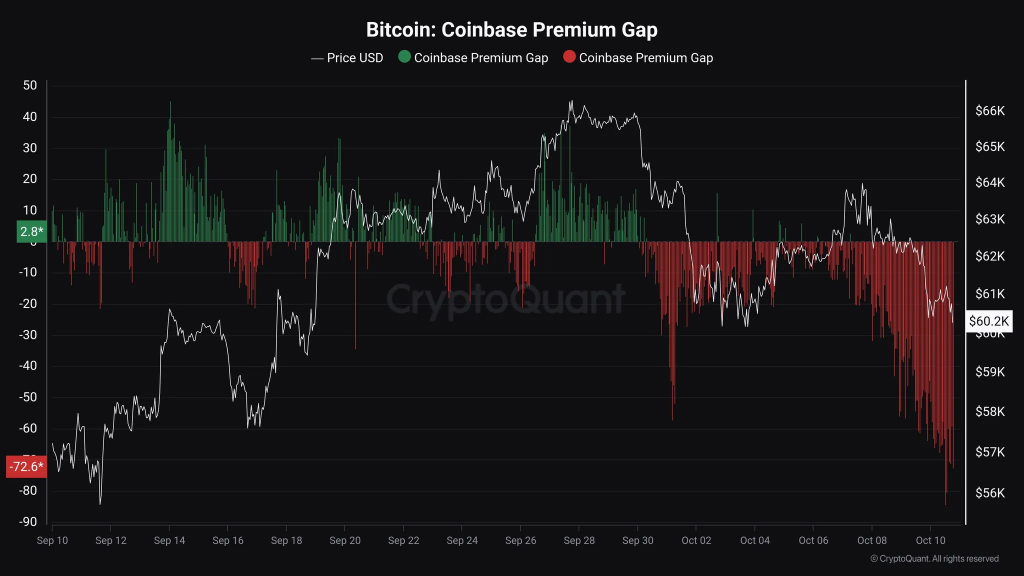

BTC defending 60k can be considered optimistic, but the CB premium of -$80 is clearly a cause for concern. In yesterday’s drop, BTC broke below its October 3 low and made another low, but altcoins including ETH and SOL did not break below their October 3 low. BTC has been moving sideways since the halving, but I think the sideways movement will end soon and a trend/expansion movement will likely occur. Summer is over, Q4 has started, and there are many uncertainties and volatility factors. It would be strange for the market to not move. [Further decline is certainly possible until the end of October, and anything below 55k would definitely be bad]

My view is clear. I feel like the market is at a crossroads… It’s a matter of life or death…

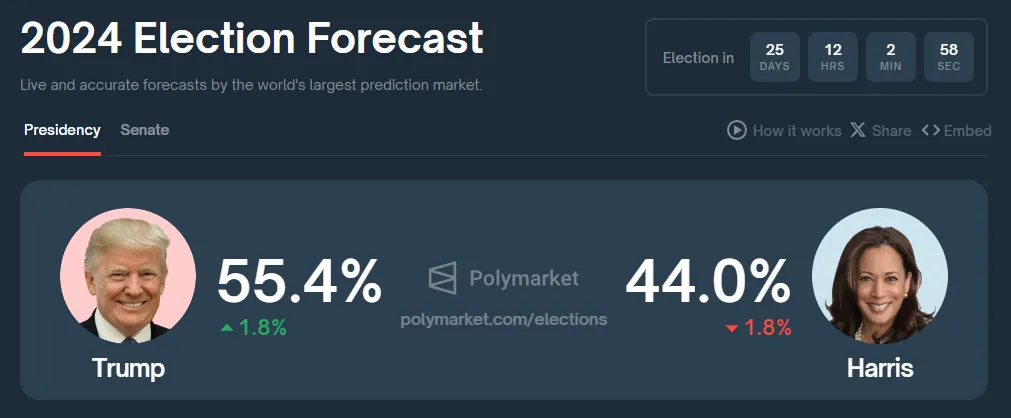

Everyone has forgotten, but the US presidential election is just a month away. The stock market is showing a rise in volatility indices such as MOVE and VIX, which means there is a lot of uncertainty. It is definitely positive that the Polymarket data shows that Trump’s chances of winning are increasing. The BTC-Trump correlation has disappeared, but who becomes president seems quite important at a time when there are no positive catalysts for BTC…

NFA DYOR

<Source : MacroMicro, Goldman Sachs, Liz Young Thomas, Kathy Jones, Maartunn, PolyMarket>

Comments