Memo for the last week of August

I want to give you a rundown of the key events and key takeaways that will be announced in the coming days and weeks. Most analysts will probably be focusing on the events leading up to September 6th. I see these as puzzle pieces for an upward rally.

I have been saying clearly for several months that the most important macro data in the market is not prices, but labor & growth. My base case is that there will be no recession in 2024, the economy will be resilient, and consumption will be solid. I am conducting my analysis based on that perspective. If you have been following what is going on, I believe you will understand.

1. August 28 – NVDA Earnings

This is an event that the market has been waiting for for a month. NVDA is currently the leader in the AI sector. It will be a very important earnings for the stock market and the current meta. Earnings are important, but guidance and what the CEO says will be more important. Most people expect NVDA earnings to be bad, but I think it will be average or at least not bad. It is not easy to predict, but the Q2 Capex of mega cap companies does not feel like NVDA’s earnings will be seriously bad. The implied volatility in the options market is expected to move around 10%.

If NVDA’s performance is bad, the market will definitely fall. If the opposite is true, the market will be positively affected by the resolution of uncertainty. Watch the market reaction.

2. August 29 – GDP

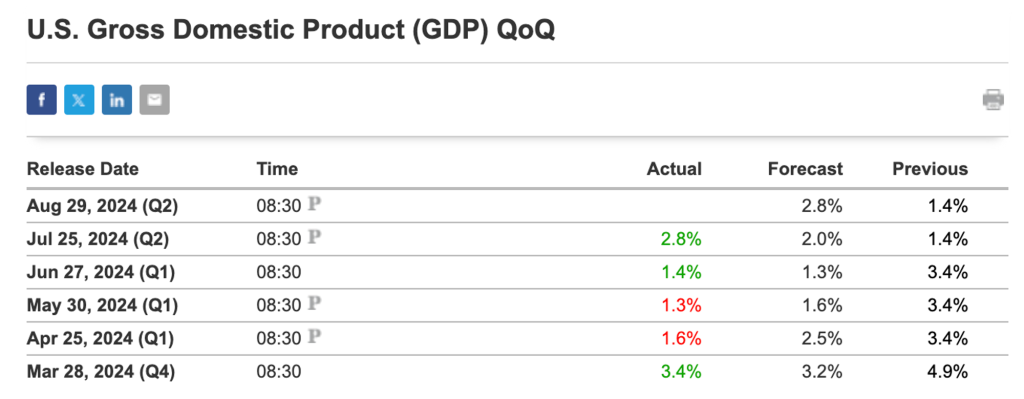

Key data. As ‘Prometheus Reserach’ points out, the key point is that the current US economy is growing, albeit slowly. Atlanta Fed GDP Now is currently +2.0%. To be honest, I don’t think GDP will be announced at +2.8%. If the data is between 2% and 3%, I think it will be a very satisfactory result, and if it is announced at 1.x%, which is below 2%, I think the market will be a little worried.

But what is clear is that if the current goldilocks situation of disinflation + nominal growth continues, it will be positive for risk assets.

3. August 30 – PCE

As you can see in the picture, the decline is slowing down, but disinflation has been going on since last year. Many people said that inflation would rise again and crash the market, but that did not happen. The core of PCE is the key, and it would be positive if the figure is lower than the YoY (2.6%) reported in July. Looking at recent economic data, it does not seem likely that inflation will increase sharply. Because of the solid disinflation trend, inflation-related data is currently less important among macro data. However, it is definitely one piece of the puzzle.

4. September 6 – NFP, Unemployment Rate

The key data for September 6th will probably be the unemployment rate. The current unemployment rate is 4.3%, which has the market a little bit worried about a recession. There was a lot of debate about Sham Rule in the market 2-3 weeks ago. So the main concern of the market is whether there is a recession or not. The labor data is noisy, so it is hard to know exactly how the unemployment rate will be released, but I expect the market to overreact and make it a volatile day.

Each element is important, but among them, GDP and unemployment rate will be more important because they are data related to labor and growth that I have continuously emphasized. Since the interest rate cut has now been confirmed, the event regarding the interest rate cut itself can be seen as over. I expect a positive result of a gradual interest rate cut without a recession. Supply and demand and liquidity are everything in the asset market. Ultimately, if the interest rate cut is a bullish event rather than a bearish event, I think there will be an expansion phase leading to a small-cap rally like the current IWM. If we overcome all these hurdles, I think the market will have a strong rally atmosphere as we head toward the end of the year.

As long as future events and data are positive for the market and BTC does not fall below $60,000, it seems advisable to maintain a bullish view without being swayed by any movement.

NFA DYOR

<Source : Earnings Whispers, Investing.com>

Comments