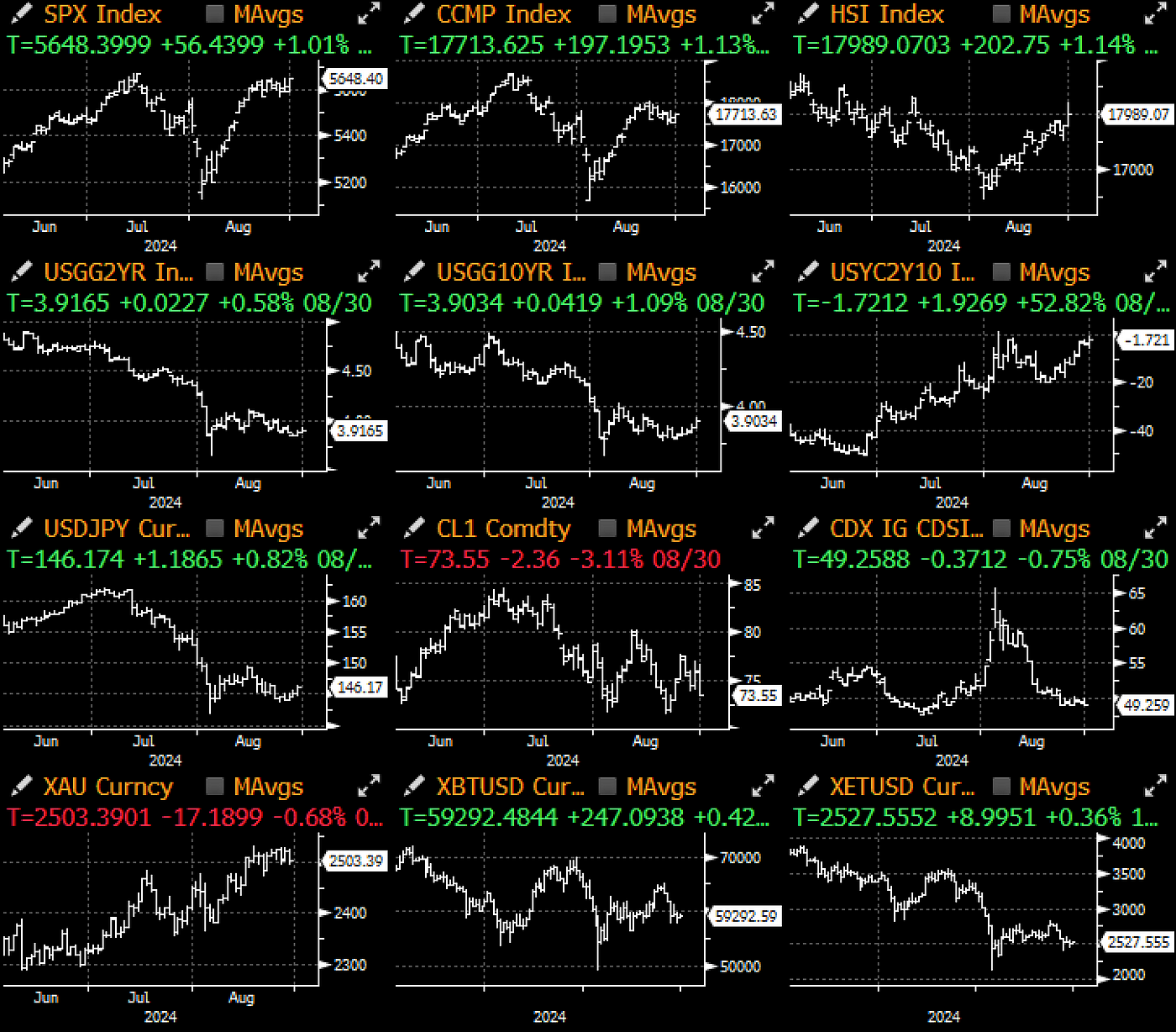

Last week was a relatively quieter week, where global equities basically retraced to their interim highs and US treasuries ending the month at the lower end of August range. Data was supportive with Q2 GDP revised up to a 3.0% handle, initial claims coming steady on a week-on-week basis, and PCE confirming inflation’s gentle slide towards the Fed’s long-term target.

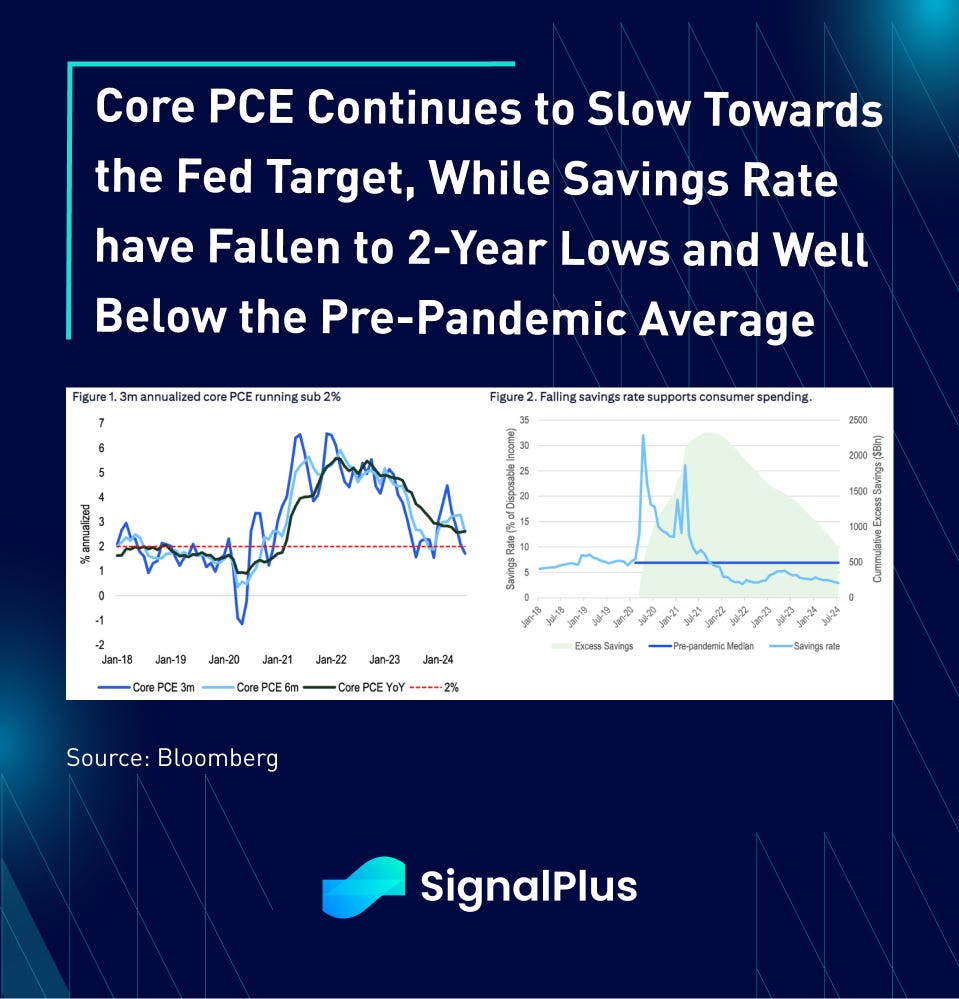

Core PCE inflation rose 0.16% MoM and 2.6% YoY, with healthy personal spending which saw another 0.4% MoM growth in real terms. However, much of the spending strength was powered by a continued fall in the US savings rate, dropping to 2.9% and sitting at the lowest point since June 2022 and below the pre-covid average.

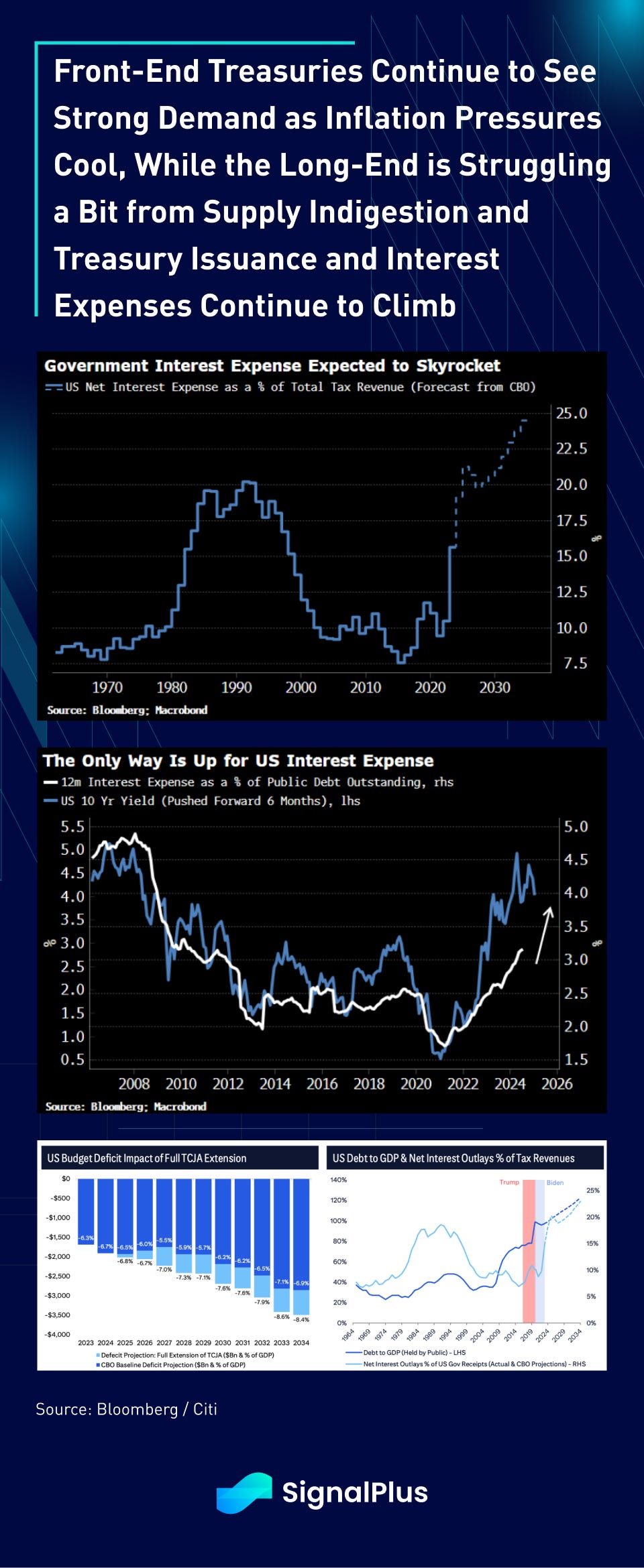

In fixed income, yields held their range this week, though the vaunted treasury yield curve (2/10s) is now a stone throw’s distance from dis-inverting after spending 2yr years in negative territory, and is the strongest sign that macro participants are now fully buying into the start of a new easing cycle from the Fed. Long-end prices are suffering from some supply indigestion, while Sept is pricing in ~33% chance of a 50bp cut thanks for falling inflation.

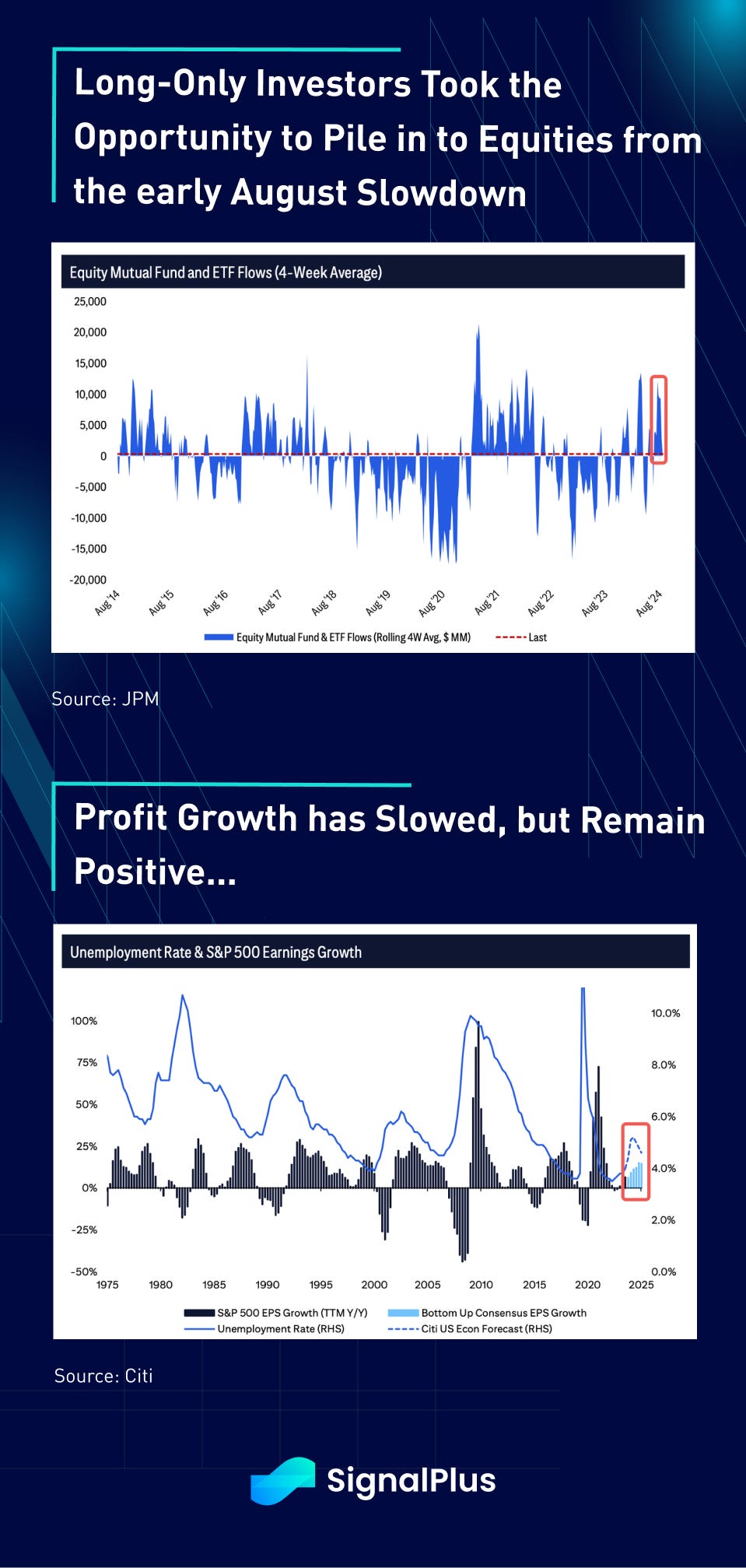

Over in equities, long-only and mutual fund investors have been large buyers of the market since the early month sell-off, and investors continue to find comfort in equities with SPX earnings continuing to grow thus far. Furthermore, underlying fundamentals remain extremely healthy as well, with both EBIT and Net Margins still rising from their historically lofty levels, as companies continue to find ways to stay profitable despite the various economic uncertainties.

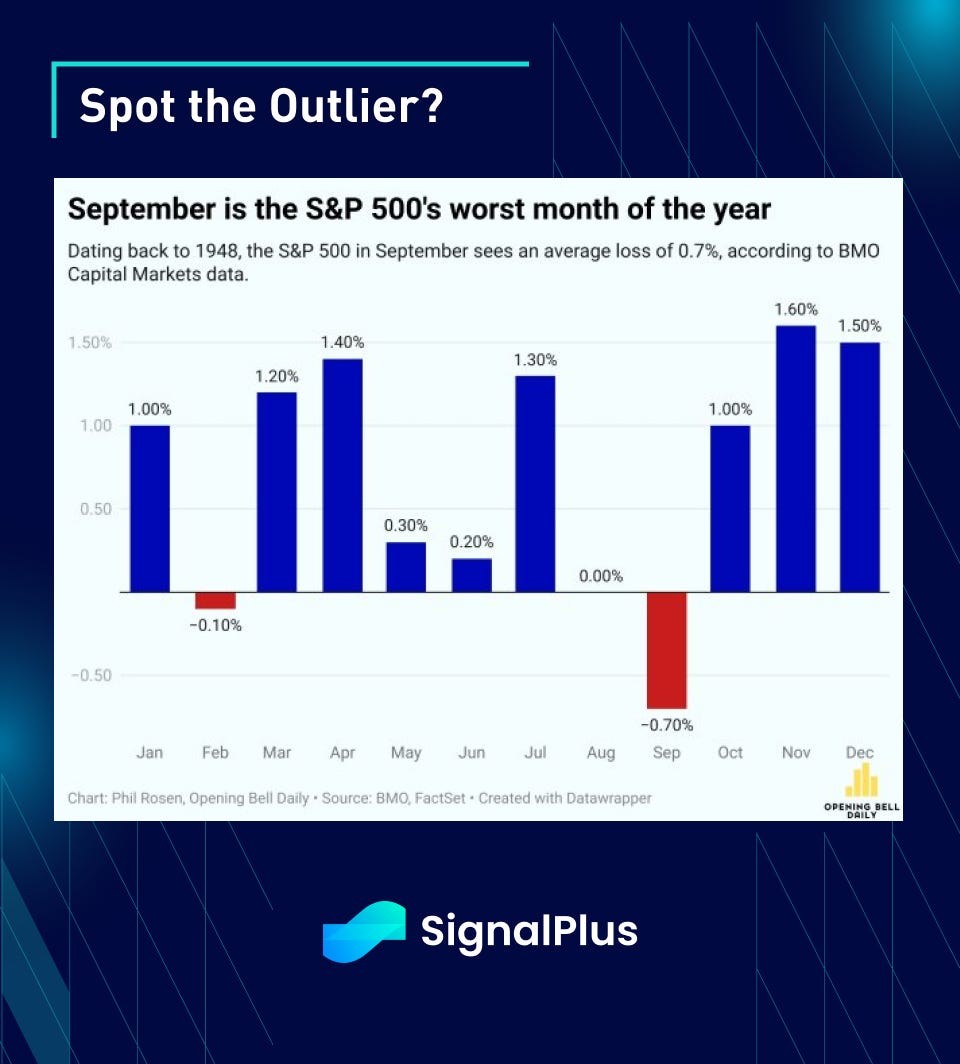

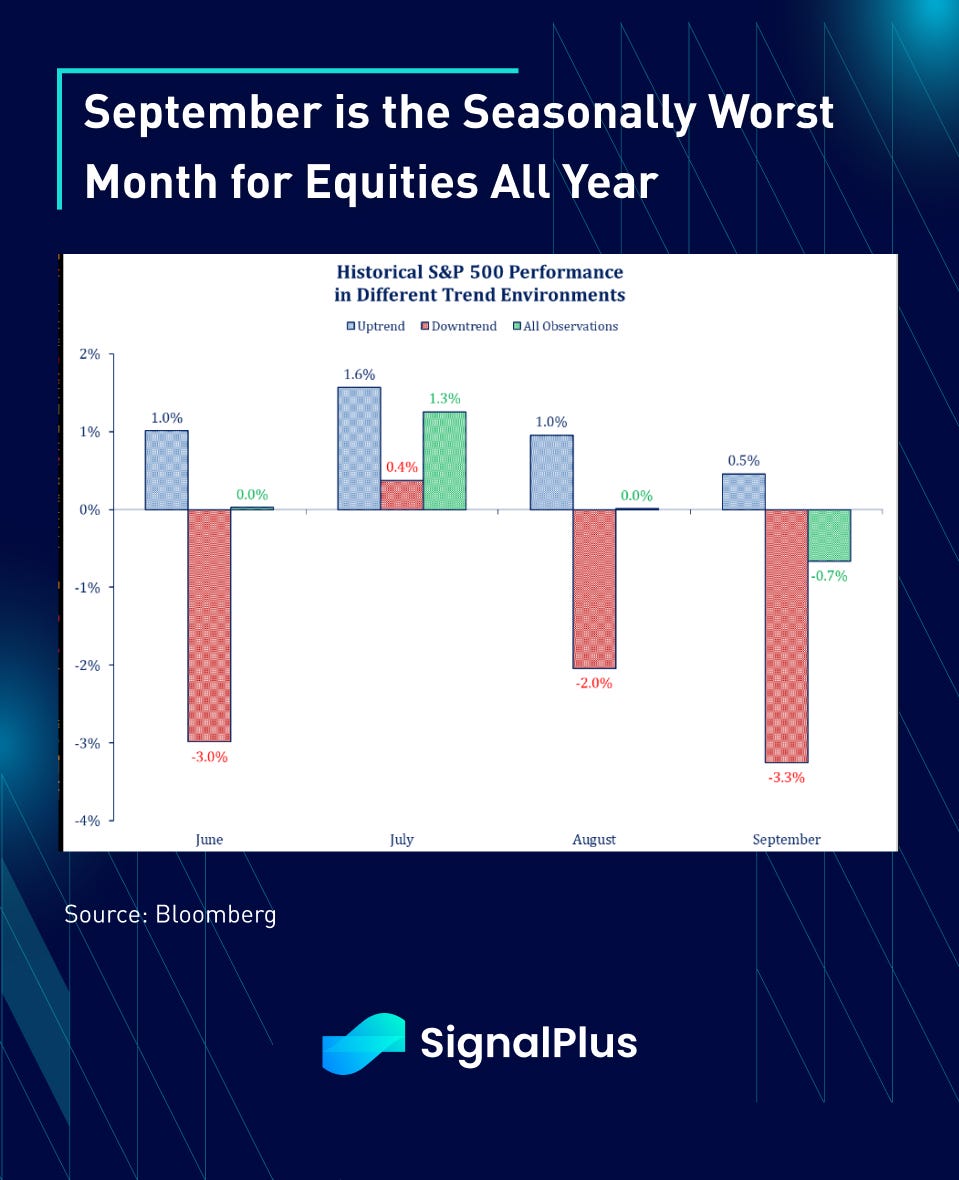

With that being said, September is seasonally the worst month for US equities during the entire year, reversing the good fortunes seen in July in the midst of summer. Will this year be any different? And will the potential catalyst come from a weak NFP to start things off in September? Will it come from a market pushback against Harris/Walz’s aggressive tax hiking plans? Will inflation be making a surprising and unwelcome return? We expect September to be a busy month, starting with this Friday’s payroll data once US markets return from their long-weekend holidays.

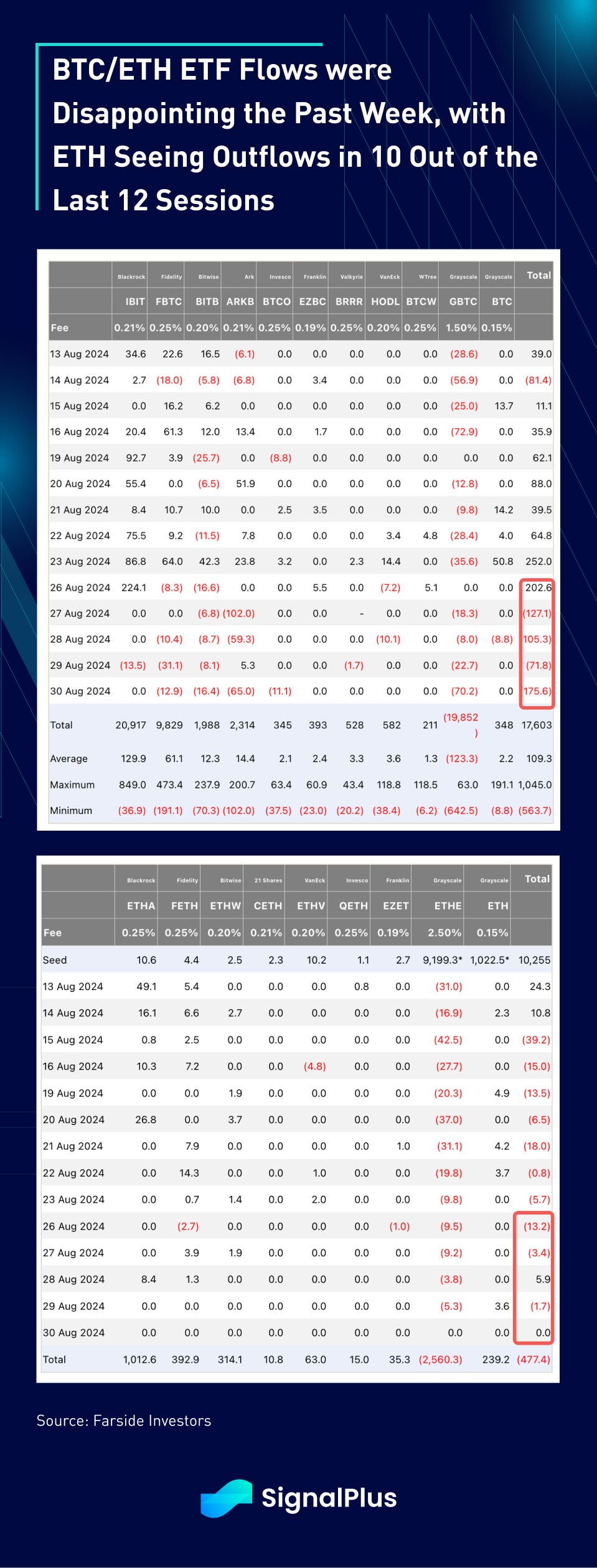

Crypto had an uneventful week but another quietly disappointing week, with both majors and alts losing around 10% on a weekly basis. Between, TG founder Durov’s arrest in France, SEC’s latest actions towards Opensea dampened the overall mood, and the continued outflows across both BTC and ETH ETFs (10 out the last 12 days saw outflows) gave markets little to cheer about.

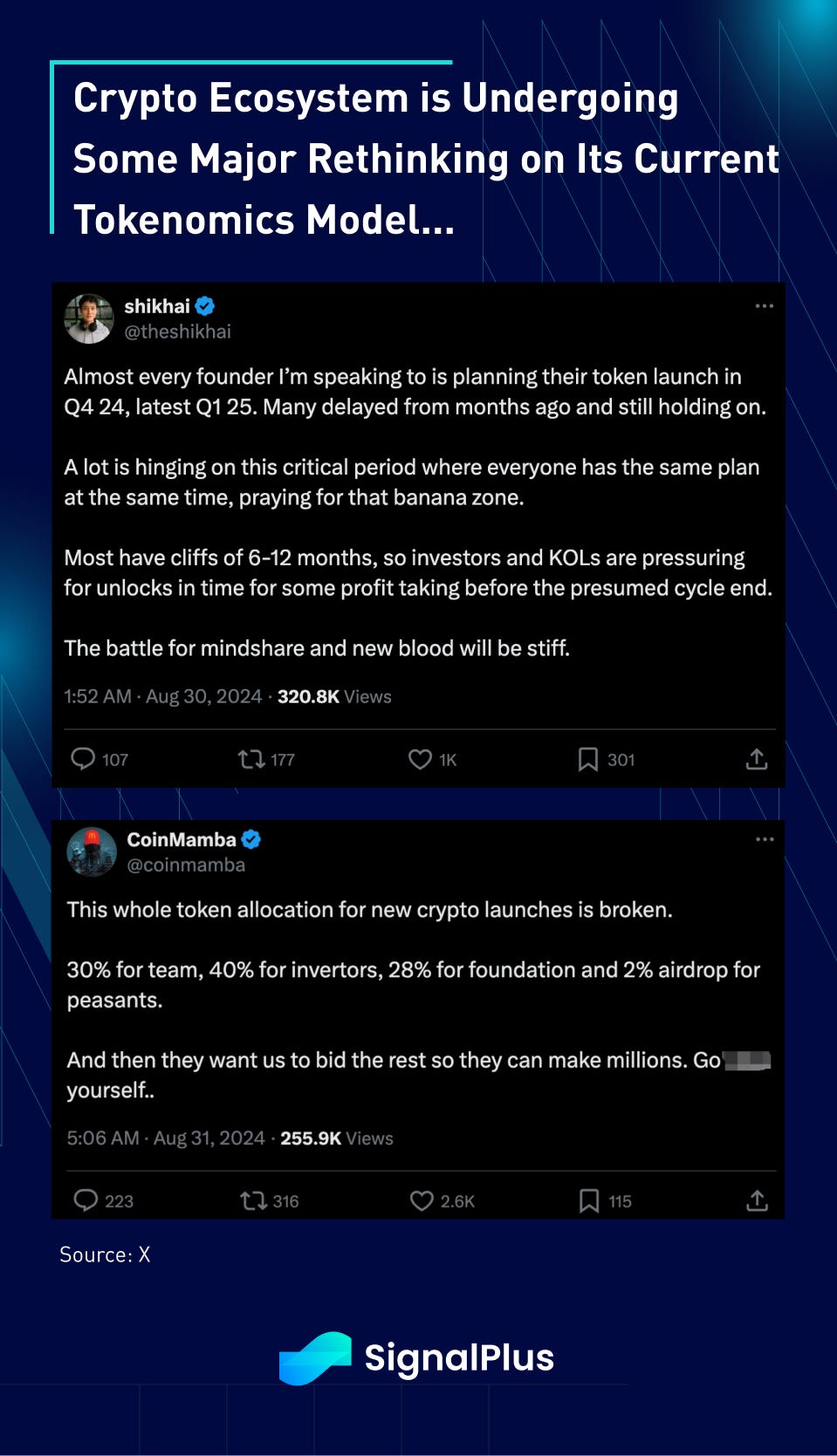

We can dedicate an entirely separate commentary towards Ethereum’s structural struggles (unattractive L1 tokenomics, over-proliferation of L2s, divergence of protocol direction from core foundation members vs users, lack of recent DeFi breakthroughs), the entire crypto ecosystem is suffering from shaky liquidity challenges (lack of exit liquidity) against what is shaping up to be a busy Q4 TGE season (e.g. Eigenlayer, Zcircuit, Babylon, Solv, Soneium, Scroll, Berachan, Monad, Gross, Elixir, Hyperliquid, Dolomite, Polymarkets, Symbiotic, Solayer… and many more).

Things certainly don’t look any easier in the near-term — stay safe out there friends!

You can use SignalPlus Trading Compass on t.signalplus.com to get more real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members:

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments