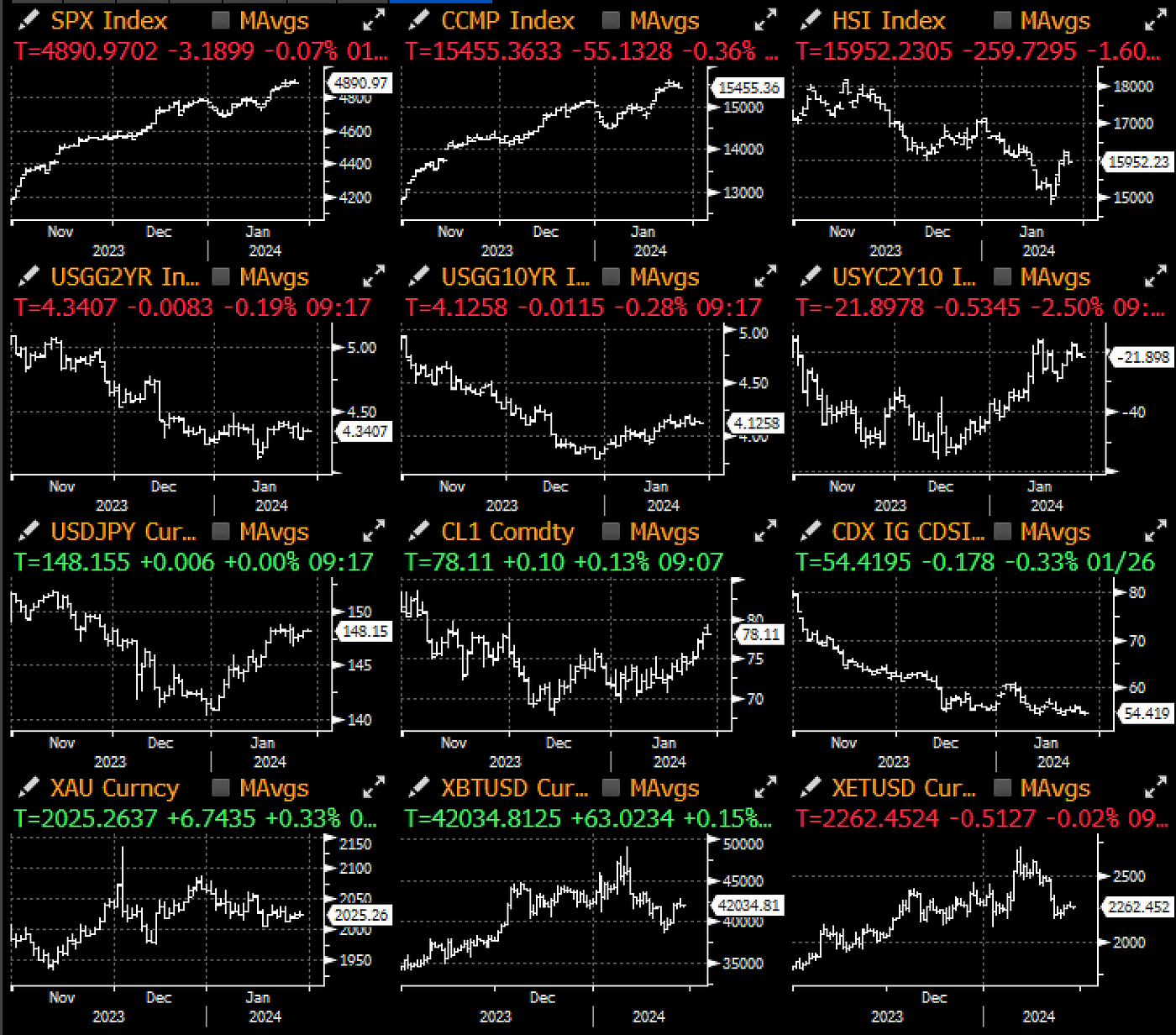

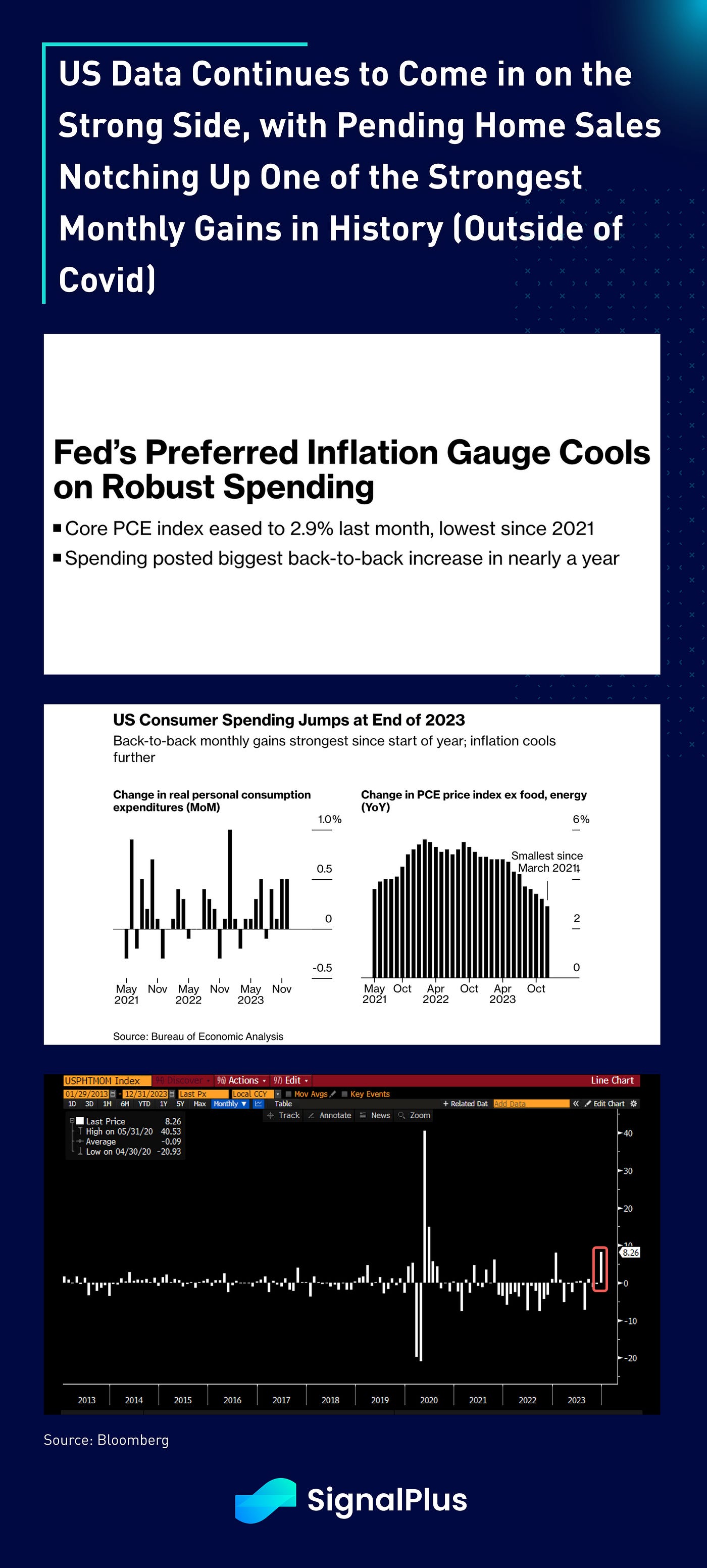

Markets ended last week on more robust US data with headline core PCE coming in at 0.17% MoM in December, though core-services remained strong at 0.28% excluding housing. Personal income and spending also came in on the strong side, while pending home sales also saw one of the largest single month jumps (+8.3%) over the past 10 years outside of the covid period.

Concerns over the underlying price strength in services caused fixed income to underperform, with investor appetite already satiated with a record $721bln of corporate issuance thus far in January. Furthermore, continued disruptions in shipping logistics, combined with an escalation in the Middle East conflicts this morning (drone attack in Jordan) are threatening to unravel some of the recent disinflationary gains with oil threatening to break $80 per barrel.

This week will mark the busiest week in macro we have YTD. Tuesday will see the release of US confidence and JOLTS job openings, followed by the Bank of Japan summary minutes, China PMI, German CPI & unemployment, US ADP, FOMC, QRA (refunding) on Wednesday, then Caixin Manufacturing, Bank of England decision, US ISM on Thursday, and finally rounded out by US NFP and U-Mich sentiment on Friday.

US earnings will have a similarly busy week with 32% of the S&P 500 reporting this week, including Alphabet, Microsoft, AMD, Apple, Amazon, and Meta.

This week features a significant amount of new information on 3 fronts: earnings, monetary policy and economic data momentum. For our outlook, payrolls are likely the most important, while the FOMC carries the widest range of outcomes and earnings may do the most to determine relative performance within a market that is higher but with risk-off details YTD. Solid news on all fronts should drive another leg higher in markets and remove excuses for caution.

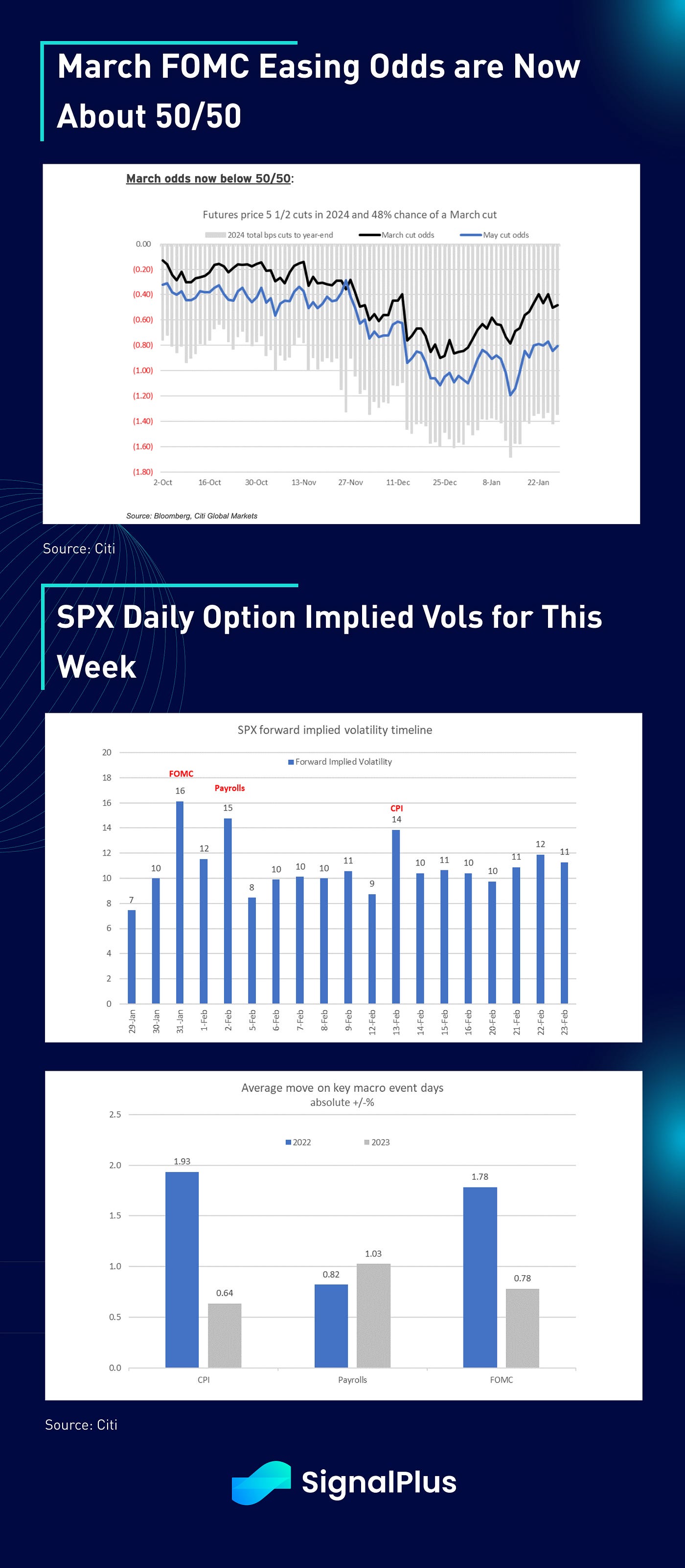

We’ll cover each of the events as they head closer, but March cutting odds for the FOMC is not split at close to 50/50, though the meeting itself might not be the most surprising event this week given it’s a ‘non-forecast’ meeting, and the markets is widely expecting the Fed to continue to manage market expectations with their current rhetoric. Citi reports that Jan 31st option straddles are currently implying a +/- 1% move, versus an average FOMC realized move of +/- 1.3% since 2022.

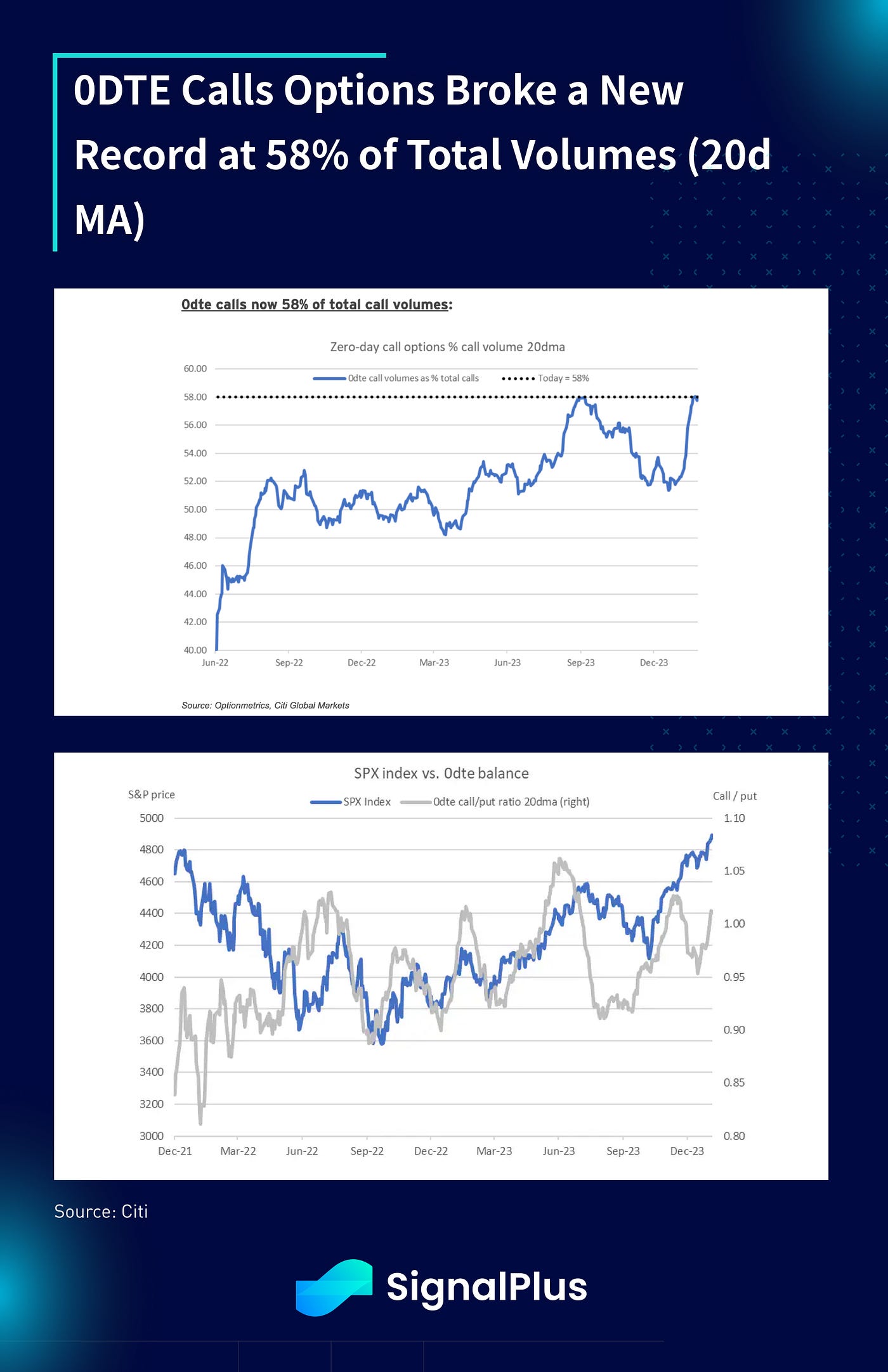

Sentiment wise, option traders remain widely bullish with 0DTE calls hitting a new record with over 58% of 0DTE volume being in calls vs puts, helping to push the call/put ratio back above 1.

Not much to update in crypto land, prices got a bump on some better short-covering over the weekend, also with news that Google will now allow certain BTC and cryptocurrency ads to be allowed through their platform, though the changes to the policy were previously announced in December 2023 already.

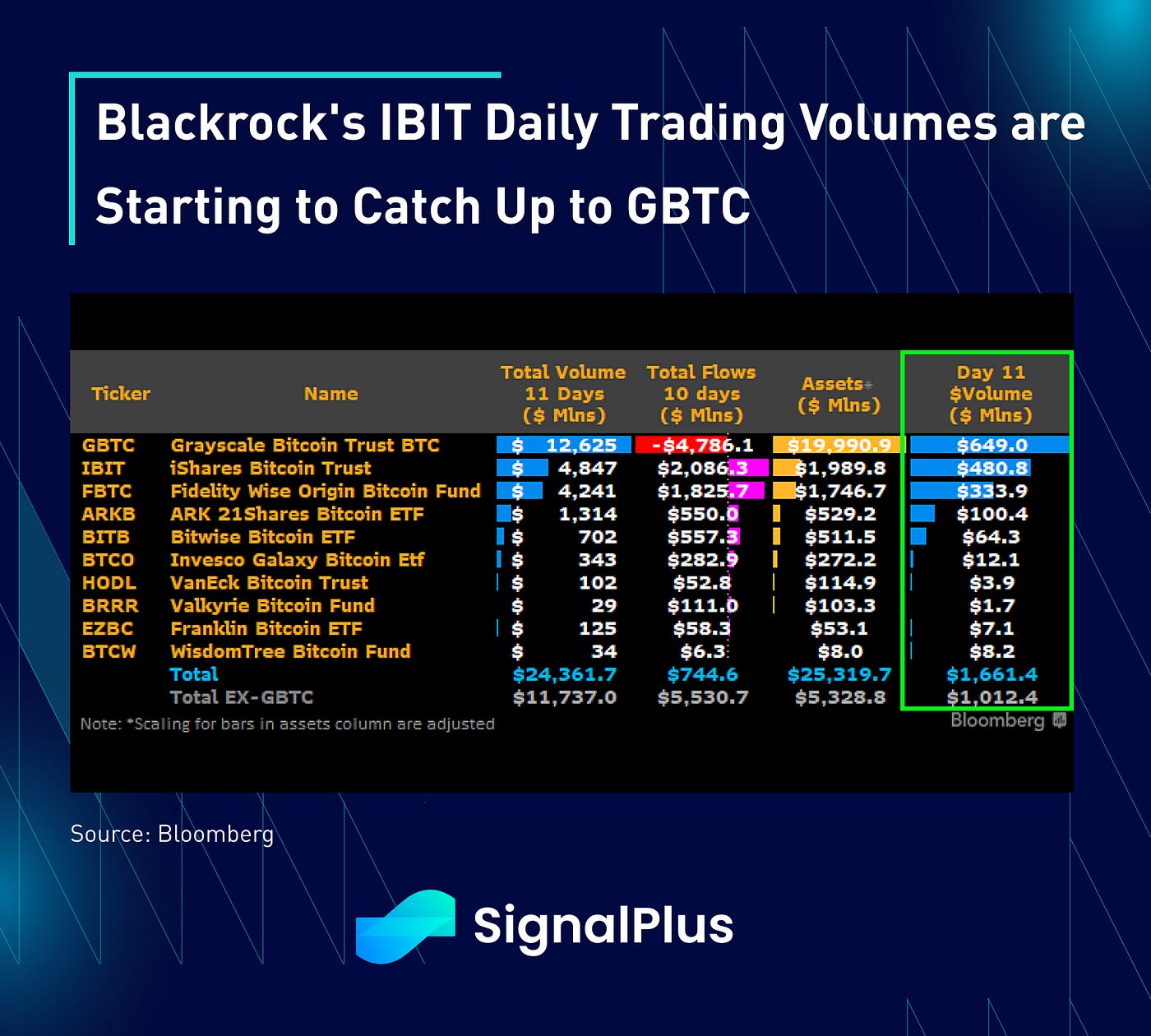

ETF flows have been more of the same before, with the group of 9 collectively serving to offset the outflow from GBTC. However, we are starting to see a real increase in Blackrock’s IBIT volume as they traded $481mm in volume vs $649mm in Greyscale, well in excess of what it was averaging over the first week of trading. Will we see IBTC’s volume flip GBTC’s by the middle of February? Will that mark the next bull market at the expense of a continued crypto take-over by TradFi? Stay tuned as we head into a busy busy week!

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Comments