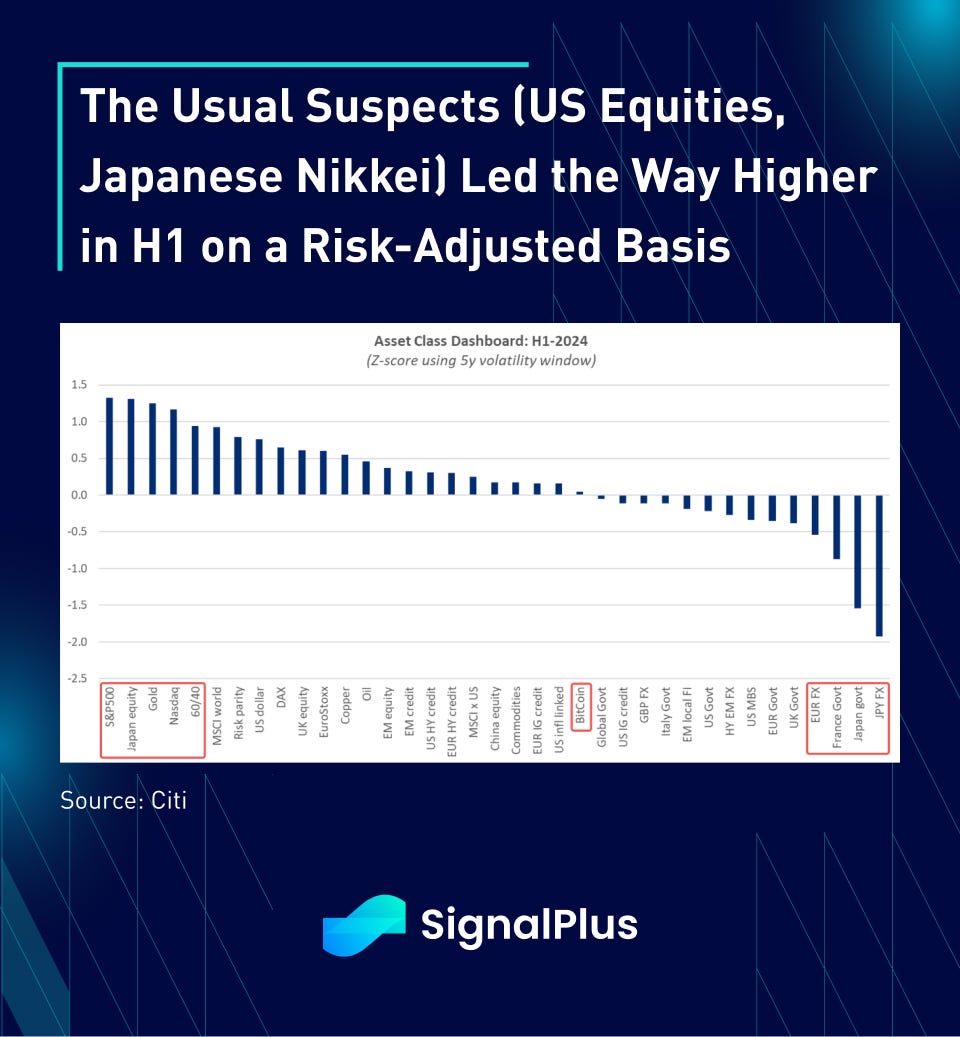

As we bid adieu to another quarter and the end of an erringly calm first 1H, a quick look at the half time report card shows the usual winners parked near the top, with SPX, Nasdaq, Nikkei, and even gold leading the pack on a risk-adjusted basis. The other side of the equation features the Yen, JGBs, EUR, and recently French OATs as the big laggards given the BoJ’s persistent zero-interest rate dynamic and Macron’s risky political gamble with the French snap election.

Not to be outdone, the USD has also been holding up strong and is at around the highest levels on an effective rate basis going back the past 30 years, thanks to continued capital inflows spurred by AI, a robust economy, and high base interest rates. US capital market exceptionalism continues to outperform the most skeptical of doubters well in 2024.

Over in EM, India continues to lead the way stronger as the capital exodus from China continues. Indian markets are up +30% (in USD terms) over the past 1.5 years while Chinese equities have sold off ~15%, for a substantial performance gap of 45%.

As we head into H2, the US election will be front and center, and I suspect another period of exceptionalism, although perhaps not the same flavor as H1. I was in the US most of last week and, naturally, the election was a big topic. I have long felt the election would be mostly about unsustainable US fiscal policy, and hence play out via the bond market, with higher yields and a steeper curve. By and large, US clients thought tariff policy would be more important, and felt a higher US dollar was the better play. While I am sympathetic to a higher US dollar, I am not sure how much more upside there is left. After all, the dollar’s real-broad index is just a few percentage points below the peaks of the past 30 years (chart below).

As we head into H2, a few clear themes are emerging:

- US economic momentum has slowed, although overall growth levels remain healthy

- The US recession remains more elusive than a unicorn sighting

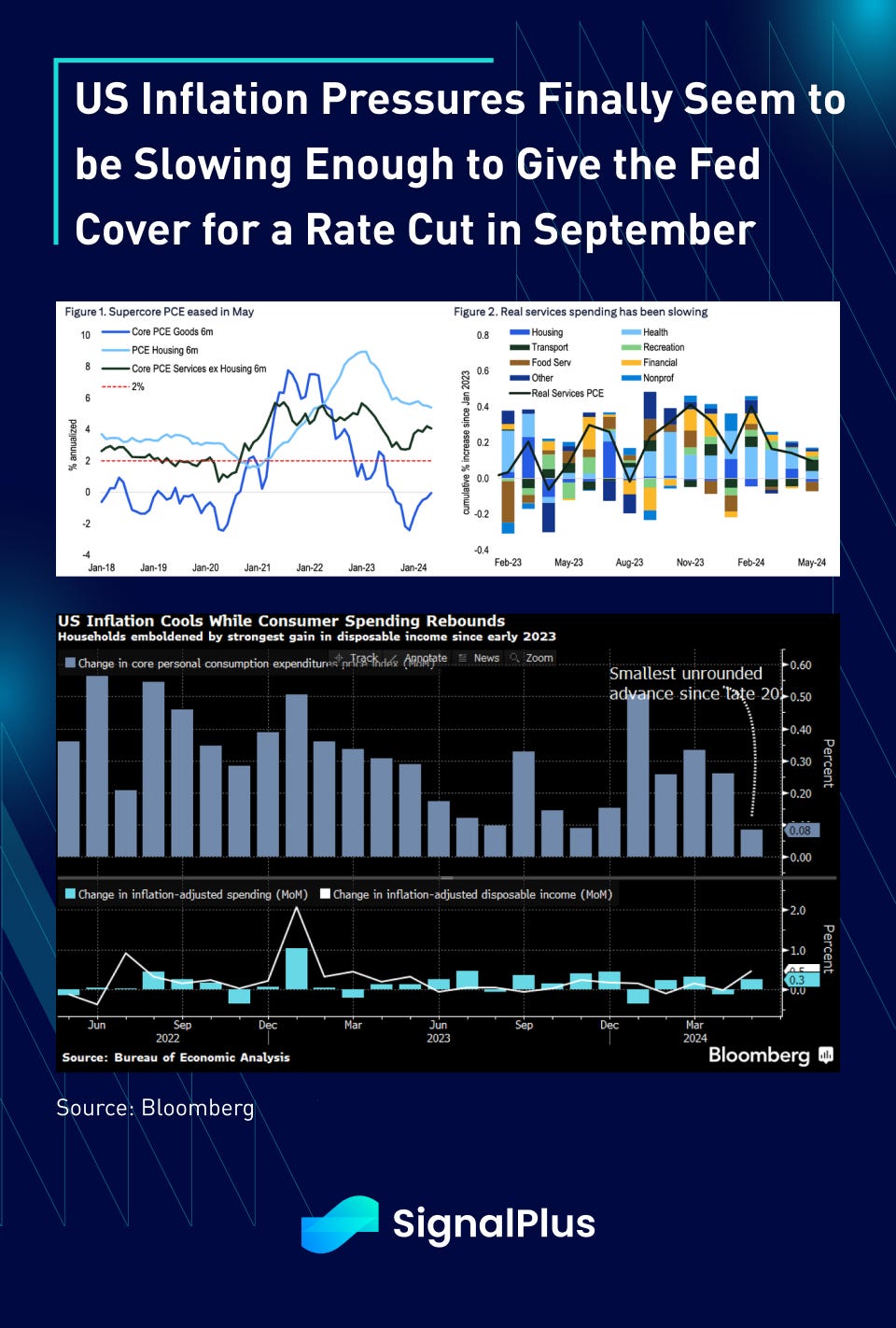

- Inflation pressures are slowing coming towards the Fed target in the right direction, but not sharp enough to justify rapid rate cuts in the short-run

- AI continues to drive overall sentiment, though there has already been some rotation / adjustments made in US markets

- With a passive Fed and an economy on auto-pilot, focus will shift towards politics with US election, fiscal spending, new tariff policies, and treasury bond supply dominating the investment narrative

On US data, it is no undeniable that the US economy has slowed from its lofty levels over the past 2 years, with economic surprises coming in at multi-year lows, and high frequency consumer data showing a large drawdown in pandemic era savings and worrying increases in consumer debt.

However, even at their more subdued levels, economic activity remains at a high level compared to previous cycles, with this week’s NFP still expected to come in at around 190k with a 4% unemployment rate and still a positive growth in average hourly earnings of 0.4%. At the current pace, 3m average payrolls are still coming in at around 249k versus an average of 181k in the 2010–2019 pre-pandemic period.

Next, on the inflation side, pricing pressures appear to finally be slowing down after a lot of stop-and-go disappointments. Friday’s PCE release rose 0.08% in May, softer than consensus expectations with ‘supercore’ PCE up only just 0.1%, helping to crystallize a Fed rate cut that looks likely to arrive in September.

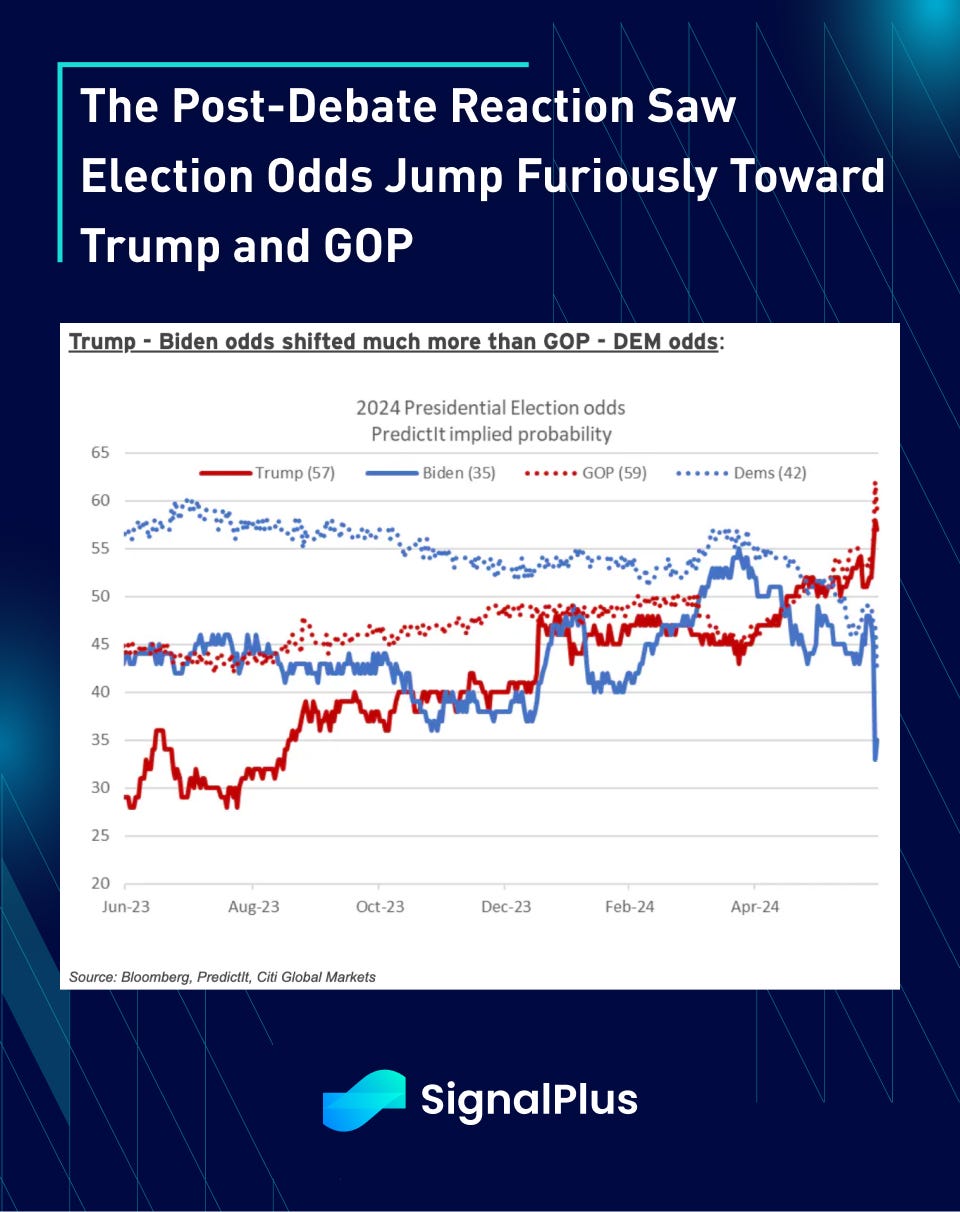

On the politics front, the 1st US presidential debate started with some excitement as President Biden delivered an underwhelming performance that was worse than the lowest of expectations given concerns over his age and health. On the other hand, former President Trump delivered a relatively controlled performance (by his standards), with the post-debate reaction swift and significant as the Trump-Biden election odds widened to +22 points vs +10 prior to the debate. Beyond the head to head, Biden’s odds (35%) are now -7 points below the Democrat’s odds of winning (42%), while both Trump’s and GOP’s odds are now coming in substantially above 50%.

A dominating win by Trump will likely have far reaching policies regarding US-China tariff policies, fiscal spending and tax cut extensions, monetary policy and Fed independence, and possibly even a crypto framework this time around.

Meanwhile, round 1 of the French election went to Le Pen’s National Rally group as expected this weekend, with the far-right group winning 34% of the national vote and is on pace to gain a parliamentary majority.

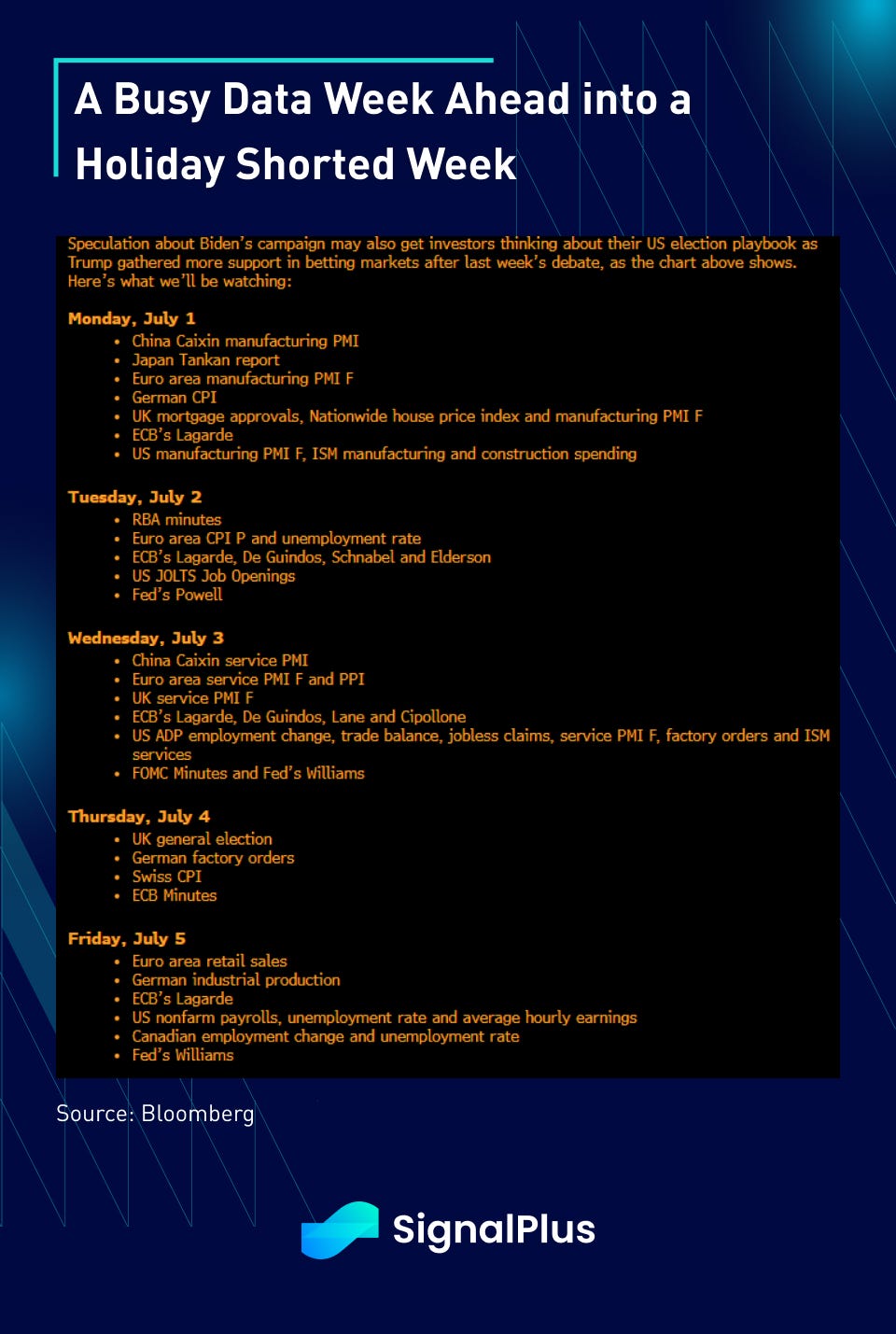

This week will be a substantially holiday-shortened week with just 3.5 trading days, and a lot of data crammed into a busy Wednesday with ADP, jobless claims, ISM services, and FOMC on the docket. This will be followed by NFP on Friday, right after Thursday’s Independence Day holiday, so expect US trading desks to be thinly staffed.

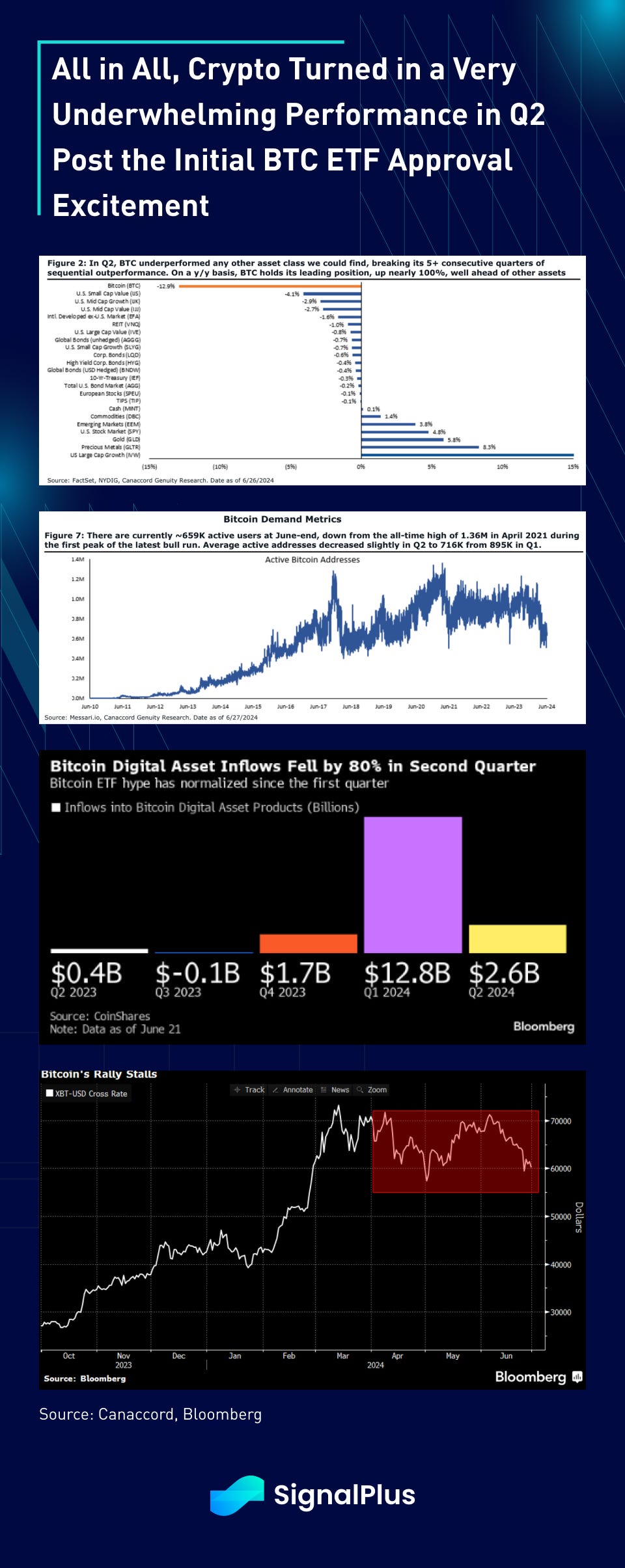

On crypto, Friday ended a very disappointing quarter with BTC registering a -13% loss for Q2 following a long period of outperformance, as slowing digital inflows, lack of substantial mainstream tech innovation, falling demand metrics, and pending supply concerns (Mt. Gox, govt sales) added to crypto’s owes with BTC unable to break out of the 60–70k range.

Ethereum was similarly disappointing, with expectations of its own ETF approval failing to draw up any long-lasting excitement over the OG mainnet, and concerns about L2 activity cannibalization and dwindling fees / inflationary supply (L1 fees plummeted to historical lows last week) continue to raise existential and long-term structural questions from the community towards the Ethereum foundation.

Will the expected ETF approval in Q3 and legal wins against the SEC (on staking) bring about any change of luck for ETH? Will a Trump victory be the panacea for the industry’s adoption woes? Only time can tell…

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments