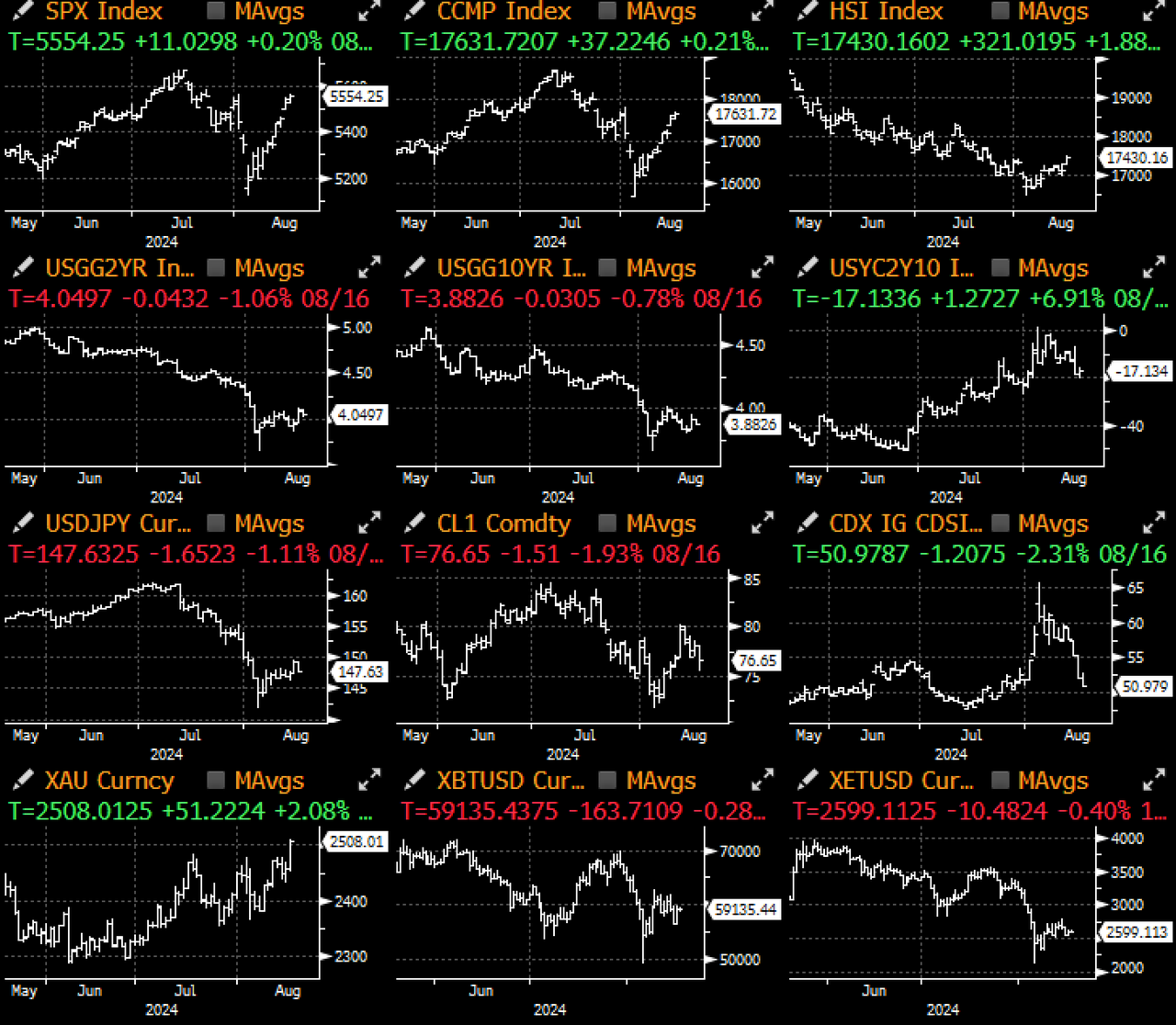

So after a turbulent start to the month, we are entering the back half of the month as if nothing had really happened. Recession fears have subsided substantially thanks to strong retail sales (+0.3% MoM for control group with a strong June), falling jobless claims, and robust corporate earnings to put markets back on ‘soft landing’ watch.

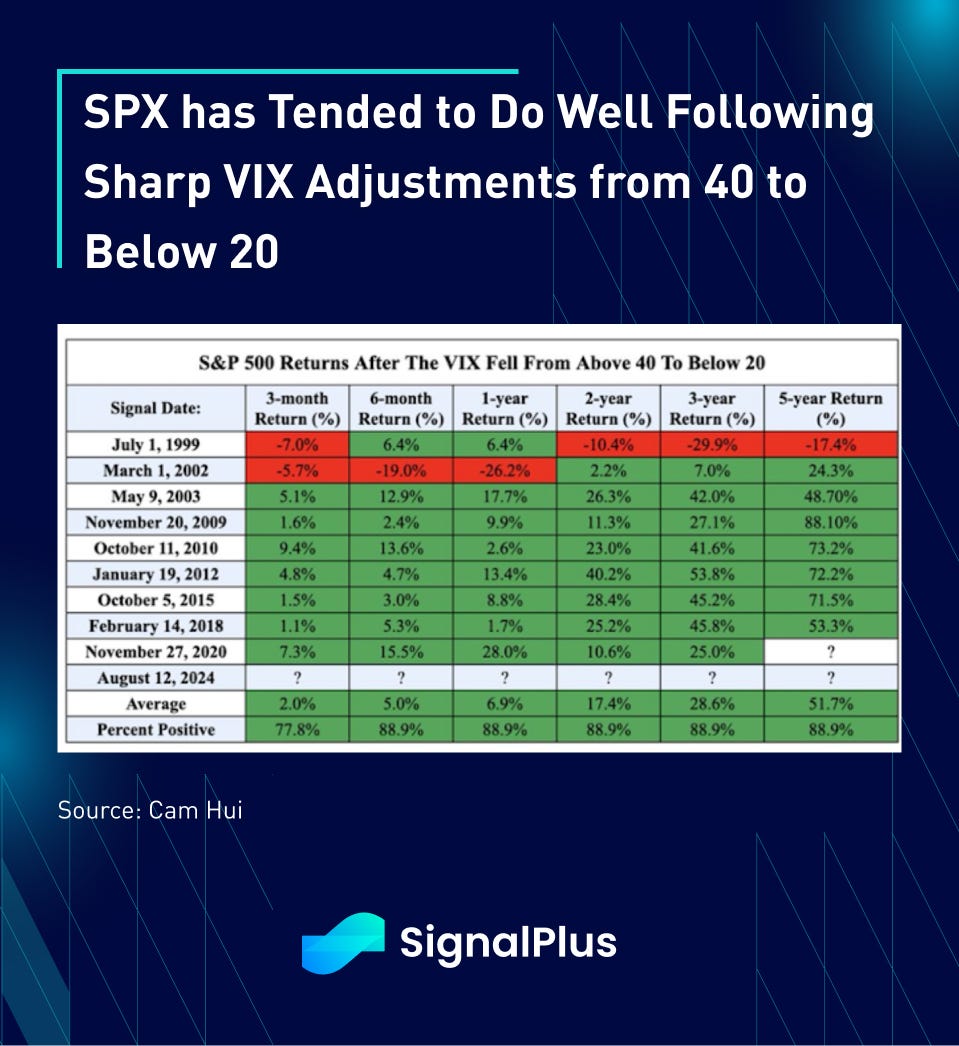

Furthermore, according to Bloomberg data, the SPX Growth index outperformed Value by more than 4% over the past week, something that has only happened 31 times over the past 20 years, with a >70% record of seeing a market rise the week after as well.

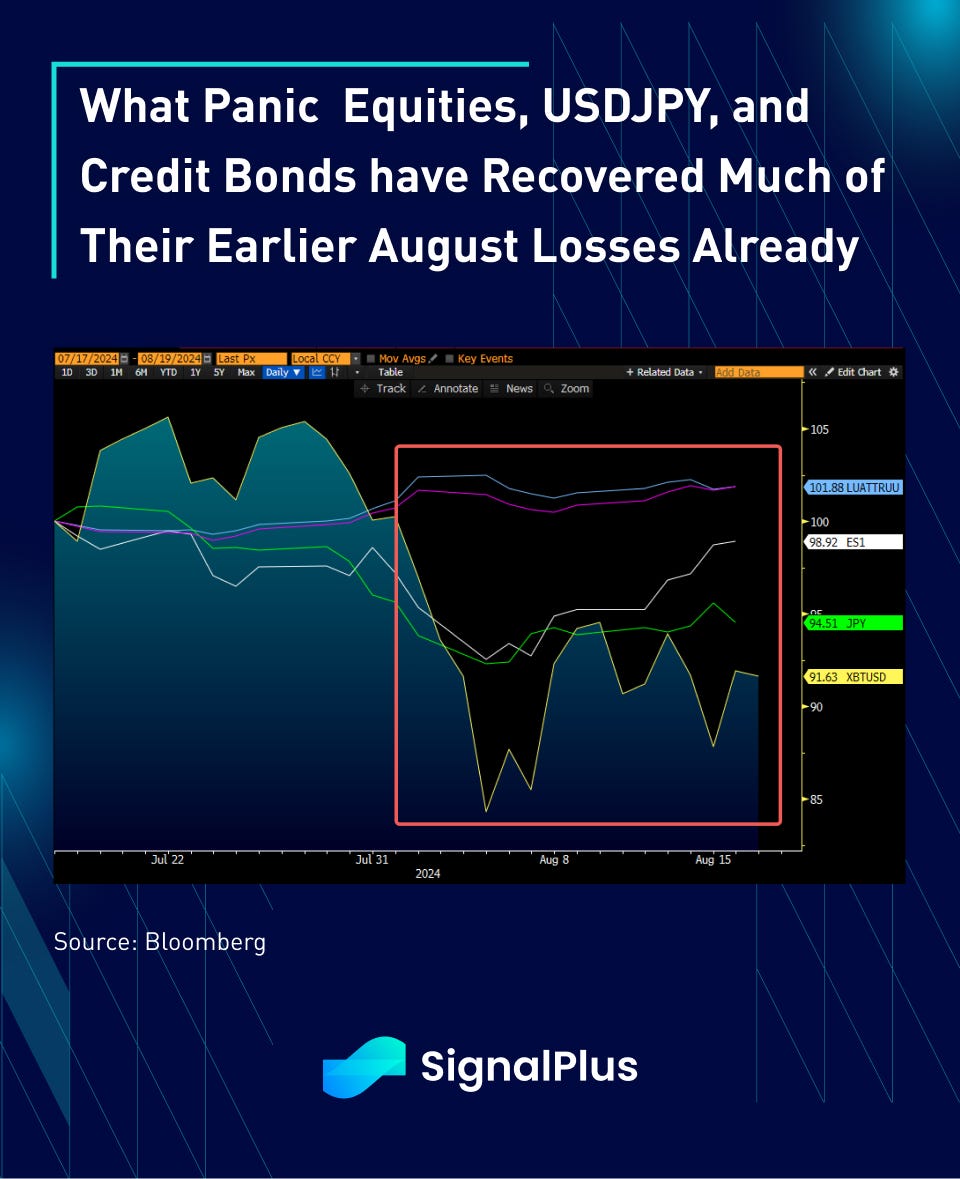

In fact, market internals (as measured by new 52 week highs vs lows) saw little panic throughout the entire move, confirming once again that the exaggerated sell-offs were driven by position and PNL stop-outs, rather than any changes in the fundamental long-term views.

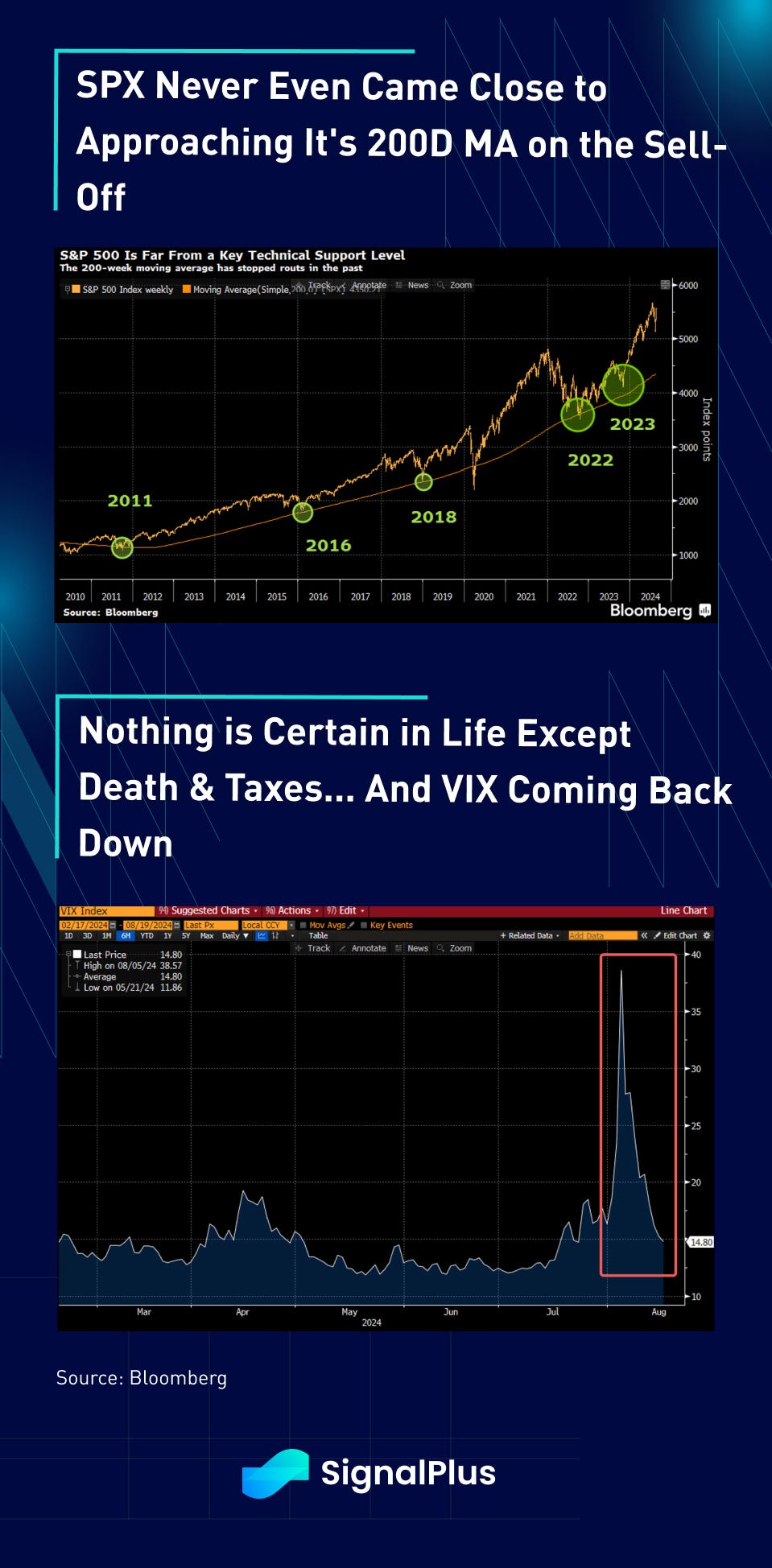

Furthermore, position estimates from Citi confirm that hedge-funds have been doing the bulk of the de-risking in August, with their positions being taken over by ‘long-only’ (LO) funds on the subsequent dip buying. If we were to extend out the horizon, one would be forgiven for barely noticing the sell-off ‘blip’ on the longer-term SPX chart, with the VIX already collapsing back close to YTD range after barely a one-week flash.

On a bottom-up basis, Walmart earnings cheered on markets with better than expected results and a rise to FY2024 guidance, with the stock jumping +7% after results. Other consumer names such as Home Depot and Starbucks also outperformed on the week, further allevating concerns about any major consumer spending slowdown

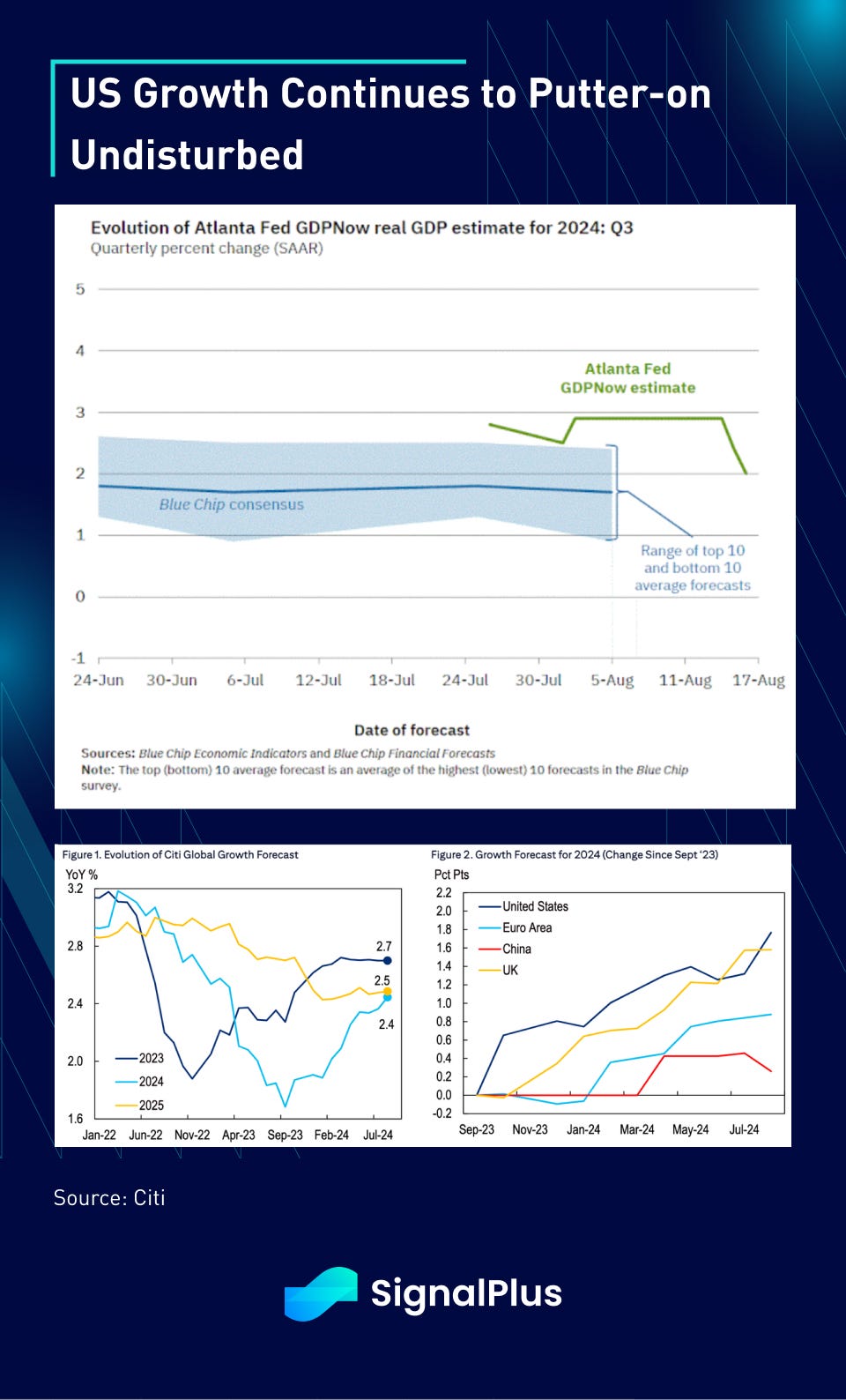

All-in-all, Q3 GDP growth has been pretty consistent over the past 2 months, with Atlanta Fed’s GDPNow barely budgeting from the 2.5%-3% area throughout this whole ordeal. Furthermore, Wall Street continues to expect the US (and the UK) to lead GDP growth in 2024 at a ~2.4% annualized rate, with 2025 rates maintaining a similar level thanks to a supportive Fed.

Now, what has changed vs July are Fed rate cuts expectations, where the market is still pricing in close to 4 hikes by December, and a 30% chance of a 50bp cut in September. However, with the rapid pace of market recovery and robust economic data, the Fed might not see much pressure to pivot as dovishly as they felt from two weeks ago, leaving the market in a bit of a vacuum as asset prices revert to waiting for more data.

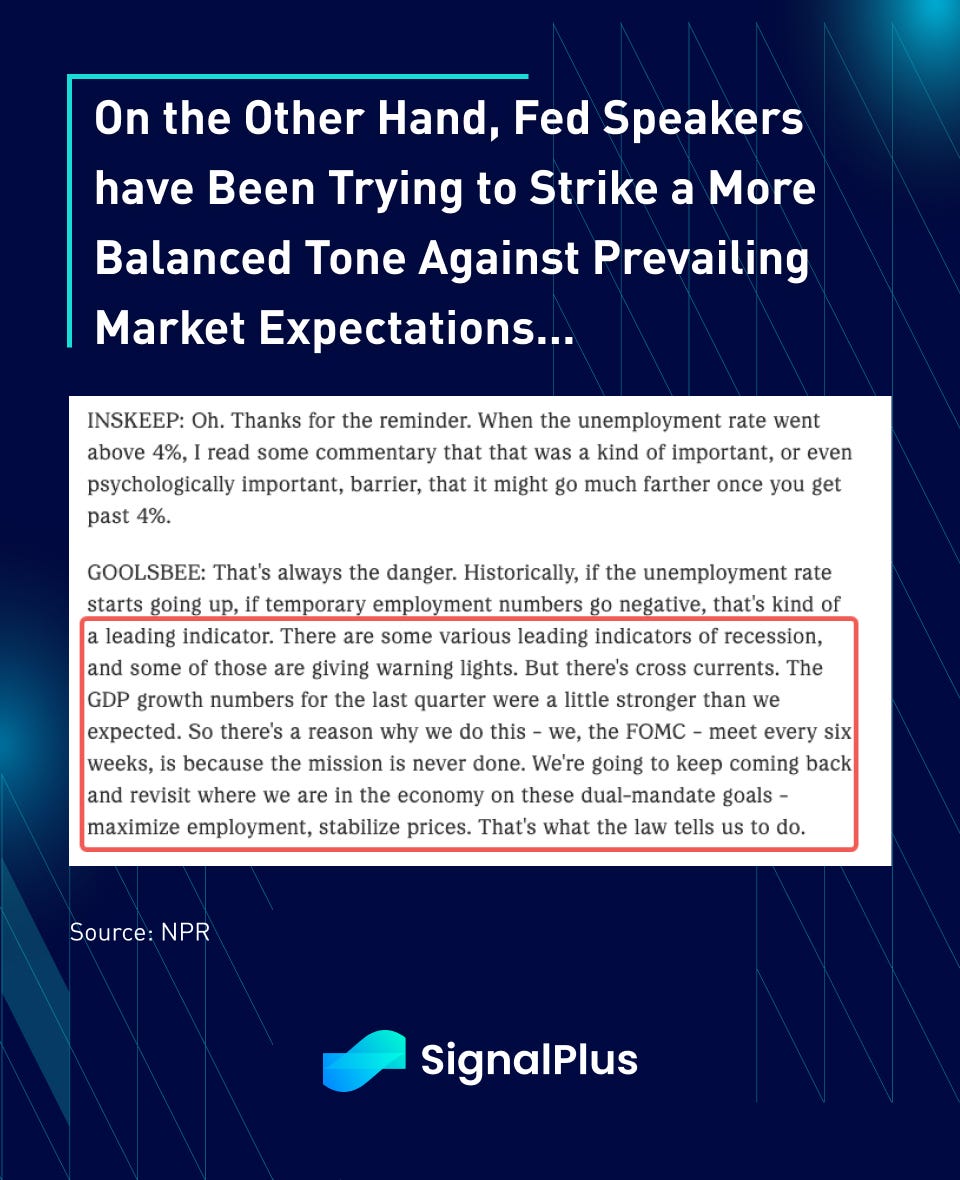

In fact, Chicago Fed’s Goolsbee, a noted dove, struck a noticeably cautious balanced tone in a recent interview that the Fed should not be over-reactive to merely some indicators of a recession. As such, this does leave the market some room for disappointment should Powell decide to strike a more neutral tone in the much anticipated Jackson Hole against market expectations. Namely, Powell can merely endorse the start of a gradual easing campaign while dialing back expectations of a 50bp move against the rapidly easing financial conditions. He can also emphasize focus away from a single disappointing NFP, while keeping an option to accelerate the pace of cuts should labour markets deteriorate more suddenly.

We expect Powell to try to walk a fine line here, and perhaps disappointing rate markets slightly on any significant near-term eases.

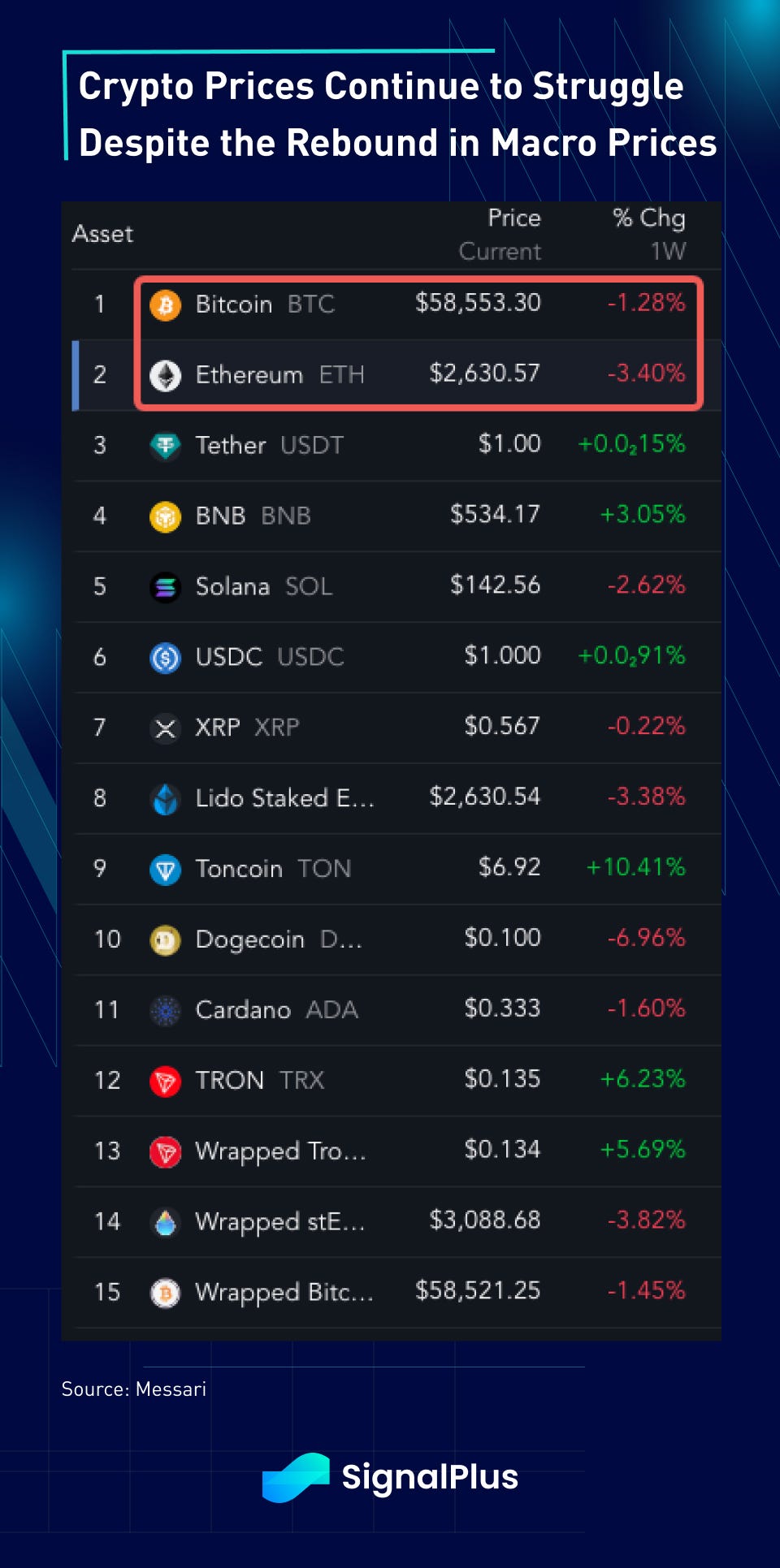

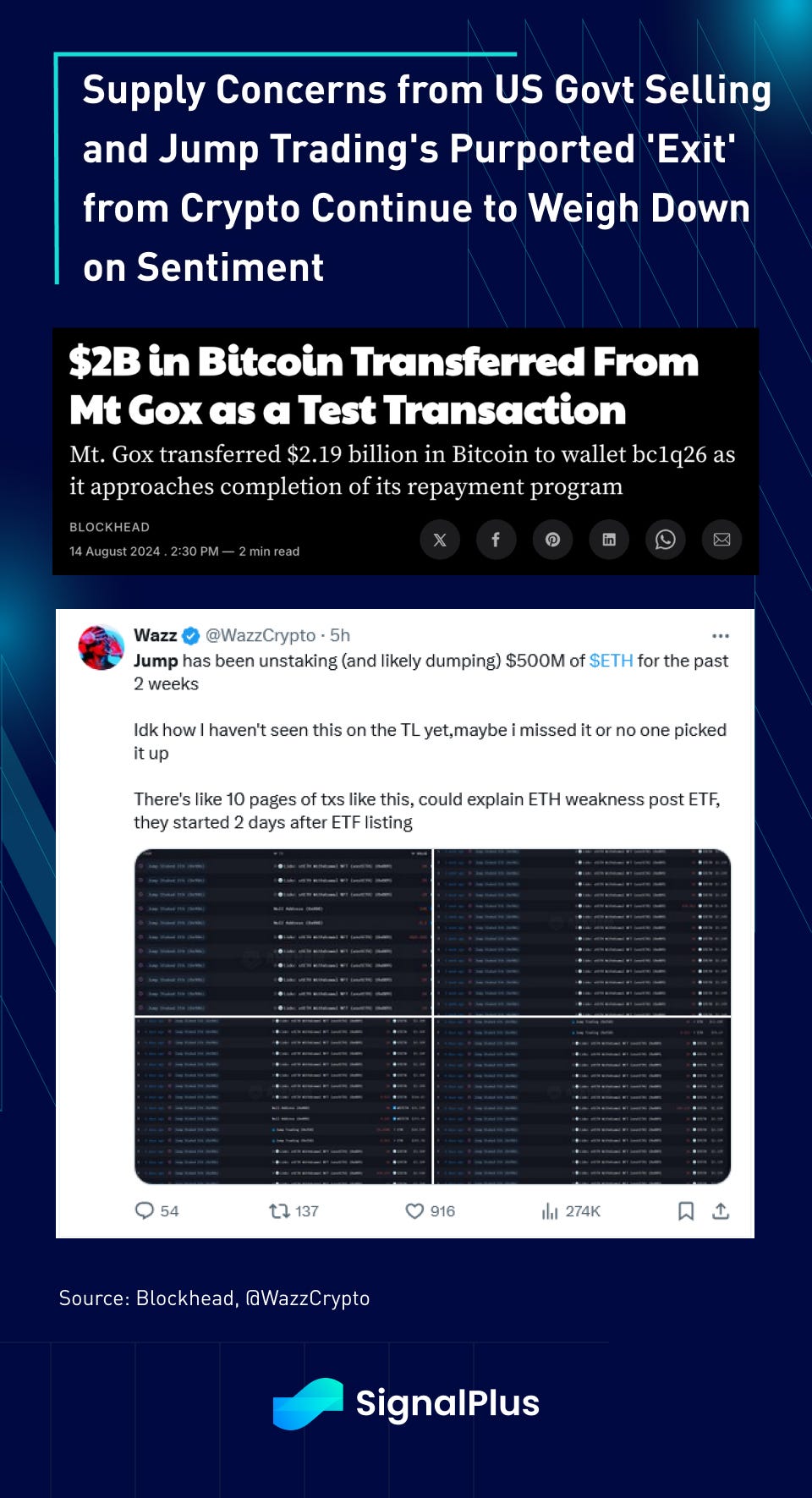

In crypto, majors are still lagging behind the recovery in equity and risk prices on the back of supply concerns from the US government (Mt. Gox) and Jump’s continued retreat from crypto. Jump was reported to have moved another 17K ETH from Lido and redeemed about 25k of wrapped ETH into stETH as the firm continues withdrawing assets to CEX to prepare for a likely unwind.

As an aside, a lack of ‘crypto discussion’ between Elon and Trump’s interview might have also disappointed listeners who were hoping for more supportive (ie. pumping) rhetoric coming from the former President.

We expect prices to remain challenging into after September, where we expect continued improvements in macro sentiment to finally pull crypto prices higher, especially considering the current light positioning against recent long liquidations, and the Fed to finally embark on their rate easing program.

You can use SignalPlus Trading Compass on t.signalplus.com to get more real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members:

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments